Climate risk management is becoming a fiduciary duty. In 2020, the Australian pension fund REST settled a landmark case with member Mark McVeigh, committing to new disclosure processes and acknowledging that climate change is a material financial risk to its investments.

But disclosure alone is no longer enough. Clients are paying attention to what the numbers say. On the Overshoot podcast, pensioner Sue Owen described how her UK pension fund projected just a 1% drop in returns over 40 years under 4°C of warming, a figure economist Steve Keen found repeated across multiple UK and Australian funds. The Overshoot podcast is aimed at the general public, not the financial sector. The fact climate risk methodology is becoming a story for mainstream audiences signals the issue has moved beyond the technical journals and sector-specific press. We read this as an indication of more lawsuits to come.

In October 2025, four Canadian pensioners took the Canada Pension Plan Investment Board (CPPIB) to court over its climate risk reporting, which estimated portfolio losses of just 4% over 75 years under a “hot house world” scenario using a popular value-at-risk model. Norges Bank, AkademikerPension, and AXA have all flagged the same model for producing implausibly low estimates because it ignores systemic risk and tipping points. The case is the first in the world to challenge a financial institution’s choice of third-party scenario models.

The recent Kvek v. Cushman & Wakefield complaint in US federal court pushes further, framing climate risk management as a mandatory ERISA fiduciary duty.

Whatever the legal outcomes of these cases, the underlying point holds for any institution producing climate risk numbers: the model you choose shapes the answer you get, and someone may eventually ask why you chose it. Which approach for which purpose? In a recent webinar, we walked through the three modeling approaches available to financial institutions and what each one can and cannot tell you. This article summarizes the key takeaways.

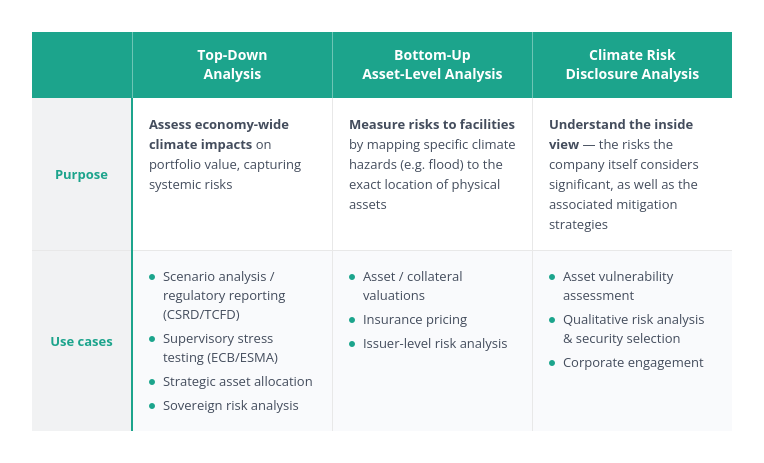

Three approaches, three different questions

Three approaches are available when estimating physical climate-related financial risks:

- Top-down macro-economic analysis

- Bottom-up analysis based on physical assets

- Climate risks disclosure analysis

The three approaches use radically different models, and serve different purposes.

Top-down analysis

Top-down analysis asks what the macroeconomy does to a portfolio under different warming and policy paths. It is built for regulatory reporting, supervisory stress testing, and strategic asset allocation. Its main strength is coverage, in two senses. It requires less company-level data, which makes it possible to assess more issuers across a portfolio. It also covers a wider range of risks than other approaches: systemic effects at city and country levels, climate tipping points, and sometimes the way markets price in future risks.

Because it integrates all these channels, the top-down approach typically produces higher impact values than asset-level methods that are more aligned with the warnings from climate scientists and the civil society. And as the CPPIB case shows, reported losses that look implausibly low can become a legal liability of their own.

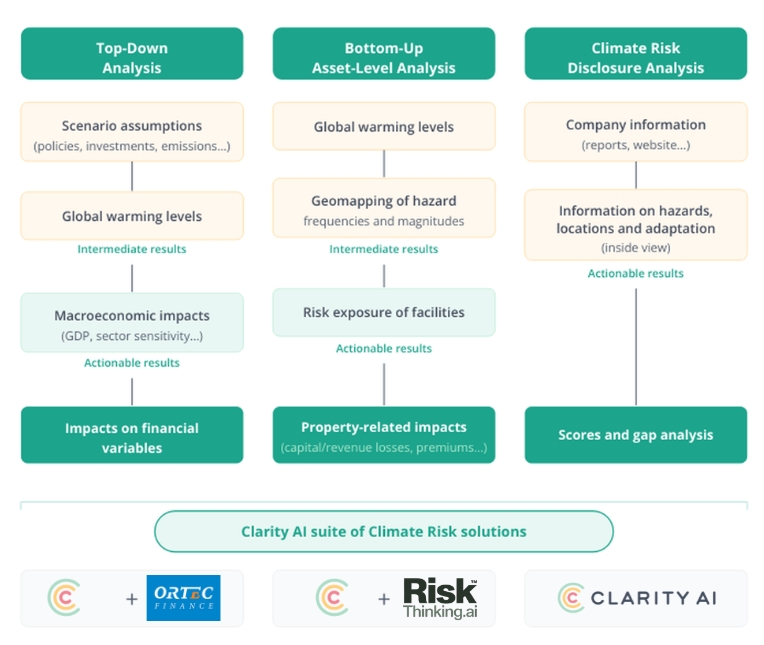

At Clarity AI, we deliver top-down Climate Scenario Analysis for 50,000 public companies and 99% of the ACWI index, in collaboration with Ortec Finance, whose macroeconomic model is built on Cambridge Econometrics’ E3ME. The model starts from real-world measurements (emissions, observed warming, energy mix, consumption, policy trends, etc.) and projects them into three scenarios: Net Zero, Net Zero Financial Crisis, and High Warming. Physical and economic projections generate emissions time series for each scenario, which are converted into temperature pathways. These pathways feed the acute and chronic risk models.

-

Acute risks: temperature pathways drive projections of extreme weather frequency and severity by region. Direct losses are estimated for the world’s 2,000 largest cities, combining historical loss and damage data with urbanization trends and adjusting for each location’s vulnerability and capacity to rebuild.

-

Chronic risks: modeled as GDP and inflation shocks. GDP shocks reflect declines in labor, industrial, and agricultural productivity, using peer-reviewed damage functions. Inflation shocks come from falling agricultural yields and rising food prices, weighted by each country’s share of household consumption spent on food and the composition of that consumption. Climate tipping points enter the calculation in the High Warming scenario.

Acute and chronic impacts are mapped to individual companies using firm-specific data (sector and energy mix, geographic revenue distribution, asset class, position size) and aggregated at portfolio level. Each scenario also embeds assumptions about how financial markets price in these future risks.

Outputs are expressed as percentage impacts on total returns across 5-, 10-, 20-, and 40-year horizons, which clients apply to their own return projections.

Physical risks are the focus in this article, but transition risk estimates draw from the same macroeconomic model, keeping physical and transition drivers consistent and allowing interactions between them.

Bottom-up asset-level analysis

Bottom-up analysis asks what specific hazards do to specific facilities. It is built for underwriting, collateral valuation, and corporate engagement, and supervisory pressure is reinforcing demand: the Bank of England, for instance, now expects banks to incorporate property-level risks into their climate assessments. Our recent partnership with Riskthinking AI covers three million assets across 15,000 companies, with precise geolocation and damage ratios across hazards and scenarios. Asset managers use this data to build heat maps of concentration risk, filter for material assets such as critical manufacturing or logistics hubs, and adjust valuations or credit models using projected repair costs and adaptation CapEx. The limitation is that direct damage measures of this kind do not capture secondary effects such as supply chain disruption or macroeconomic spillovers.

Climate risks disclosure analysis

Disclosure analysis asks what the company itself sees as material. Since TCFD introduced physical risk into mainstream reporting in 2017, and with the IFRS, ESRS, and California CARB regimes now building on that base, more companies are disclosing scenario analysis results and their planned adaptation measures. We measured that about 50% of large caps with critical infrastructure provide enough detail to map risks to specific hazards and locations. The data is rarely in a clean table; it is scattered across reports, which is where large language models become useful. The inside view adds context the other two methods cannot reach: management’s own judgment on what is material, the financial transmission channels they expect (revenue, OpEx, CapEx), and the adaptation measures they have planned. The trade-off is comparability, since scenario choices and reporting formats remain non-standardized across companies.

When the views disagree

We recently analyzed DSM Firmenich, a chemicals company, using two of these approaches. We ran a disclosure analysis on their report, and the bottom-up approach under the same scenario assumptions (high warming, medium term out to 2030). The two answers showed differences.

The bottom-up model flagged riverine flooding at a facility sitting next to a river in South Korea as the primary near-term physical risk. DSM Firmenich’s own disclosures, however, point elsewhere: extreme heat and drought at manufacturing sites in the US, France, the Netherlands, China, and Switzerland. The report maps those risks to financial transmission channels (revenue and operating expenditures) and provides tangible adaptation measures for each (e.g. water recycling). Korea does not appear in the company’s material risk disclosure.

It would be premature to say one is right and the other wrong, but the disagreement is itself information. For a portfolio manager working on stewardship, it gives engagement something concrete: “Your reports flag heat and drought at sites in five countries, our model flags flooding at the Korean plant. How do you see this, and what is the adaptation plan there?” That is a sharper conversation than the broad one most engagements settle for.

Which approach to use?

The practical question for any institution producing climate risk numbers is which approach to use. The honest answer depends on the decision being made. For a narrow technical question, one approach can be enough: top-down for regulatory reporting, supervisory stress testing, and strategic asset allocation; bottom-up for underwriting, collateral valuation, and real estate or infrastructure investment decisions; and disclosure analysis for understanding management’s view and informing engagement.

But consequential decisions raise the bar. For material capital allocation, for active stewardship, for any case where being wrong carries a legal or reputational cost, one approach may no longer be enough. Each method has known blind spots. Top-down loses granularity at the company level. Bottom-up misses value chain effects, systemic effects, and tipping points. Disclosure analysis depends on what the company has published. Running several approaches covers more of the picture, and the points where they disagree may be worth investigating too. The DSM Firmenich case showed why: each method gave a coherent answer on its own, but the discrepancy between them was where the useful risk management started.

This is the practical case for a 360° view which may also become, increasingly, the prudent approach.

Pensioners are now suing fund managers over the choice of a single risk model, and regulators are starting to ask how the numbers were produced and whether the producer considered alternatives. An institution that runs several approaches, understands where they agree and where they disagree, and can explain its reasoning, is in a stronger position whether the audience is a regulator, a client, or a court.

Watch the full webinar on demand with Jean-Charles Prabonneau (Clarity AI), Nico Fettes (Clarity AI) and Jessica Zarzycki (Nuveen).

Author Information