At first glance, recent data from the global financial sector contains a paradox: despite years of aggressive green regulations, the carbon intensity of European financial institutions appears to be rising steadily.

But this “surge” is an illusion. The financial sector is not necessarily getting dirtier; its emissions are finally becoming visible.

Exposing the emissions that were always there

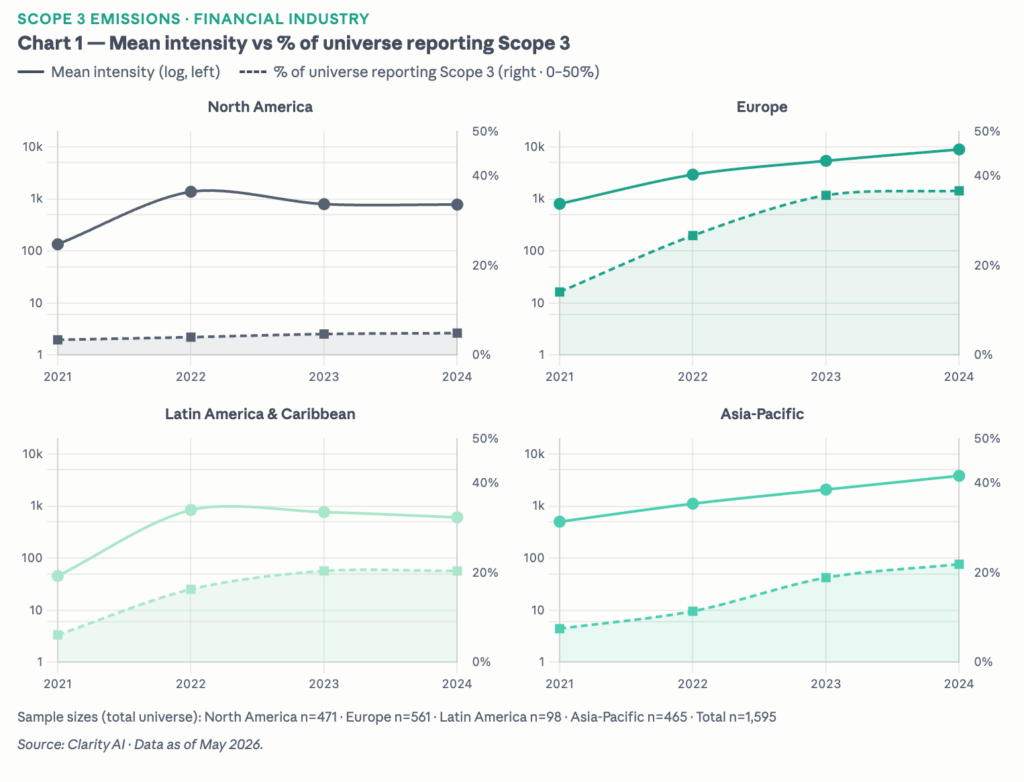

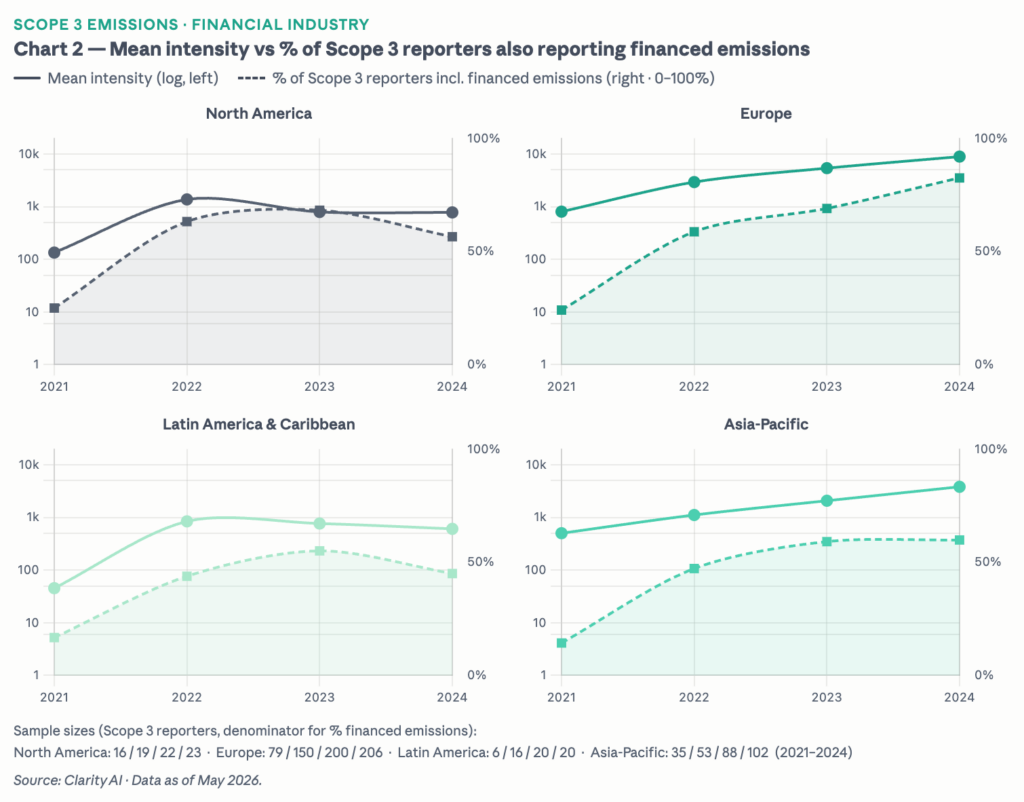

As more financial institutions report their Scope 3 emissions, we see an attendant uptick in average Scope 3 intensity across every region. The data demonstrates that this is likely due to fuller reporting, and in particular the growing inclusion of Category 15 financed emissions: the category that captures the climate impact of a firm’s loans and investment portfolios.

Chart 1 captures the first layer of this story: as the share of financial institutions disclosing Scope 3 at all increases, measured intensity rises in parallel. In Europe, that share has nearly tripled, from roughly 14% in 2021 to 37% by 2024. Chart 2 isolates the mechanism more precisely: among those already reporting Scope 3, the share that also includes Category 15 financed emissions has steadily increased, independently of how many new firms have entered the reporting pool. In Europe, that figure has risen from around 24% in 2021 to approximately 83% by 2024.

Together, the two charts point to the same conclusion: the emissions were always there. Regulation is making them visible.

The divergence: why Europe is leading

Comparing across regions, Europe is leading the way. The steeper rise in both reporting rates and average Scope 3 intensity in the EU is most likely attributable to the more mature framework for emissions disclosure across banking, asset management, and other financial sectors, which has progressively required more comprehensive reporting.

Among North American institutions already reporting Scope 3, the share also disclosing financed emissions has slightly declined, from 63% in 2022 to around 56% in 2024.

This shows the value of regulation: it doesn’t “create” new emissions, but it encourages full reporting and reveals emissions that were already there but not visible to the market.

The high stakes of a regulatory rollback

This finding comes at a critical moment for the market. Last month, the European Commission indicated it was considering a carve-out that would exempt certain asset managers from reporting on their financed emissions under the ESRS. This risks reversing the trend toward greater transparency, and could lead to the EU taking a step back compared to other regions globally in terms of reporting completeness. For investors, the extra reporting may represent burden, but it also supports their own stakeholders (end investors, shareholders and the broader public) to fully understand the emission profile of their investments.

Author Information