Data center power demand has quadrupled due to the artificial intelligence boom, but Big Tech’s reported carbon footprints are doing the opposite. Global carbon accounting rules are at the core of this inconsistency: under current greenhouse gas global (GHG) reporting standards, companies can report their electricity-related emissions (i.e., scope 2) using different accounting rules:

- The Location-Based Method: quantifies Scope 2 emissions using the average energy generation intensity of the physical grid where consumption occurs.

- The Market-Based Method: quantifies Scope 2 emissions based on the specific electricity attributes a company contractually chooses to purchase via instruments like certificates or supplier tariffs.

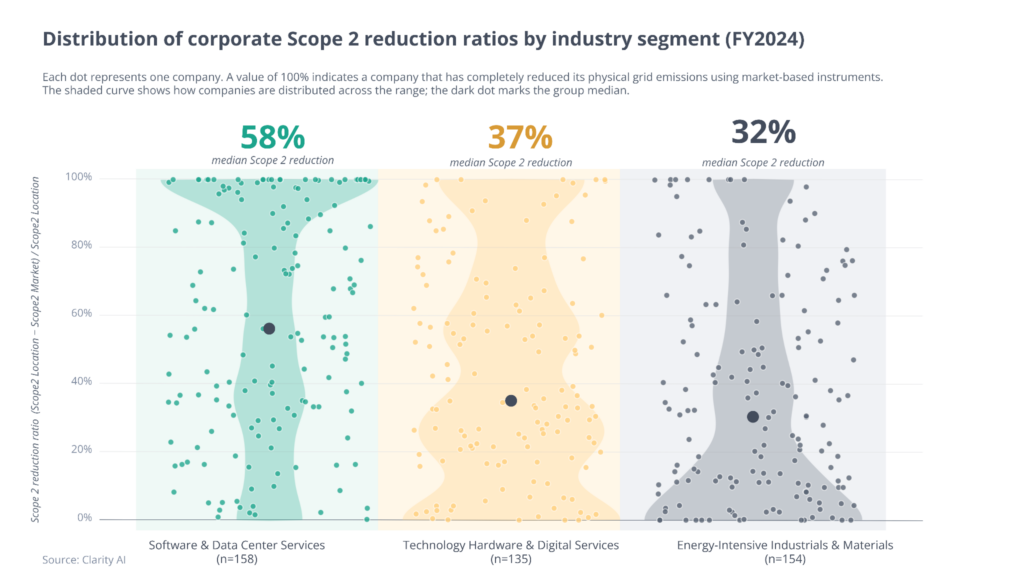

Companies are relying heavily on market-based accounting mechanisms to reduce their reported footprints. While this divergence is expanding across all observed sectors, it is more prominent in firms operating data centers1.

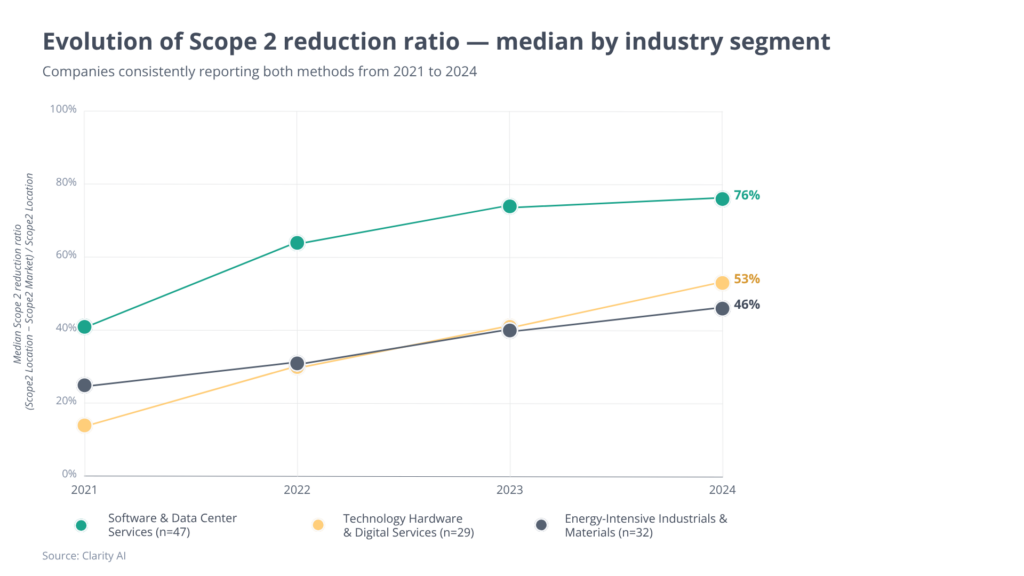

Consequently, the gap between physical grid consumption and balance-sheet reporting is materially wider for these technology firms than for their tech-hardware or heavy-industry peers2. Among a consistent panel of companies tracking both metrics annually from 2021 to 2024, the median reduction ratio climbed from 41% to 76%.

However, these companies are not decarbonising faster than heavy industry. Their greenhouse gas footprints are dominated almost entirely by electricity consumption, so reducing this footprint through the procurement of Renewable Energy Certificates (RECs) is hiding a material impact of these companies in the real economy.

Strategic Implications

Current Scope 2 accounting rules rely on the GHG Protocol’s 2015 Guidance, which permits companies to report near-zero emissions via market-based mechanisms despite relying heavily on fossil-fuel-dependent grids in reality. To bridge this gap, the GHG Protocol is actively revising these rules following a public consultation period that concluded in early 2026. If approved, the updated framework will mandate tighter temporal and spatial granularity, matching emissions claims directly to the hour and location of consumption. This shift will fundamentally disrupt traditional, annually-matched Power Purchase Agreements (PPAs), forcing a reliance on complex hourly-matched (24/7) contracts and causing a material unwind of the massive emissions reductions currently claimed by major tech firms.

Anticipating this shift, it is hardly a coincidence that Big Tech companies have announced pivots toward carbon-free energy supported by technologies that remain unproven at scale, such as small modular nuclear reactors.

Until then, investors must recognize that artificially lower Scope 2 market-based emissions among data center operators can mask a material climate risk that is not being priced in, one that will only intensify as the AI boom continues to drive global electricity consumption to unprecedented levels.

References

- Software and Data Center Services are considered as those with Global Industry Classification Standard (GICS) code of 4510 (Software & Services), including the largest firms operating data centers (90% of global hyperescalers’ data center usage, where the remaining 10% mostly corresponds to Chinese based companies that do not consistently report Scope 2 using both methods).

- Technology hardware & digital services are defined as those with GICS code of 4520 (Technology Hardware & Equipment) while energy-intensive industrial & materials are mostly chemical and extractive industries (Copper, Industrial Gases, Specialty Chemicals, Forest Products, Commodity Chemicals, Steel, Silver, Diversified Metals & Mining,Fertilizers & Agricultural Chemicals, Aluminum Mills and Secondary Production, Diversified Chemicals, Pure gold, Aluminum, Paper Products, Gold, Precious Metals & Minerals, Ore Iron Mining, Aluminum Primary Production).

Author Information