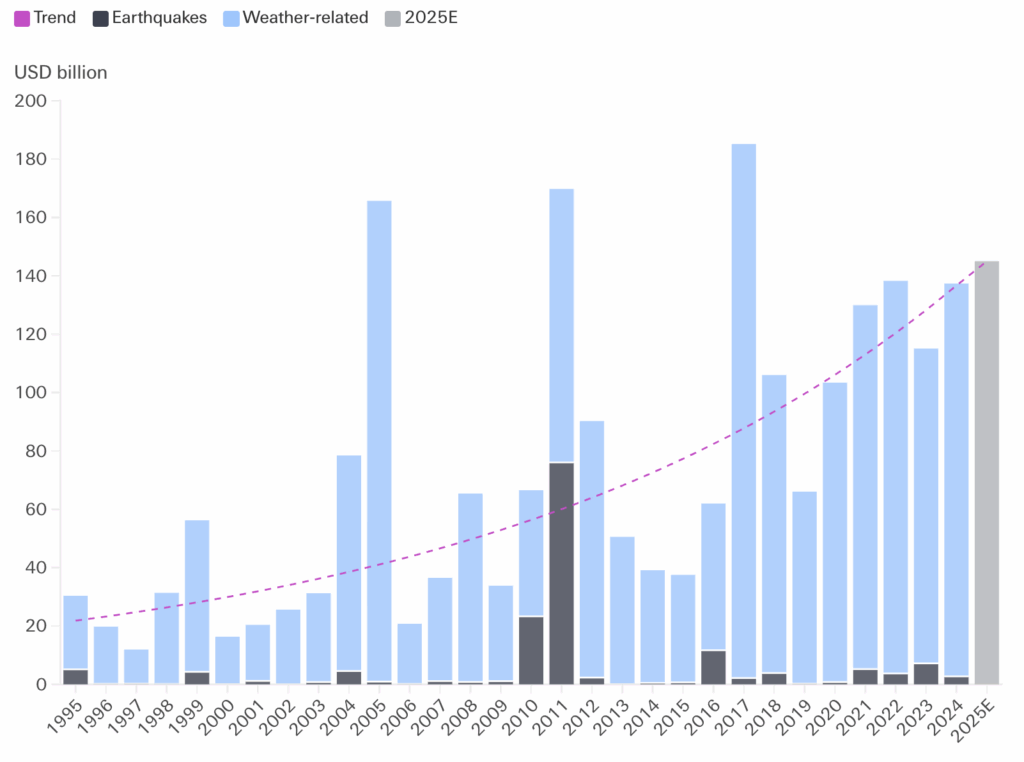

Physical climate risks are escalating globally, with demonstrable impacts on populations, ecosystems, and the world economy. As climate change progresses, these risks are anticipated to intensify. For years, data from reinsurance companies have pointed to an accelerating rise in economic losses caused by extreme weather events since the 1990s (see Figure 1).

Consequently, physical climate risks represent a category of considerations that investors must urgently integrate into their decision-making processes.

Figure 1. Growth in global natural catastrophe insured losses (2024)

Specialised tools can help evaluate their asset exposure, particularly in infrastructure and real estate, to long-term climate impacts and extreme weather events. But for corporate investments, it is even more important to understand the companies’ strategy for managing physical risks, especially for companies with complex supply chains and geographical diversification of locations and revenues. Many companies have already developed risk management strategies (for example, insurance or business continuity plans) that must be taken into account when assessing vulnerability.

A first starting point is to analyse whether a company adequately measures physical climate risks using climate scenario analysis, which evaluates potential future climate conditions and their impacts on a company’s assets and operations under different plausible climate change scenarios.

The concept of climate scenario analysis for effective risk assessment and strategic management (of both physical and climate transition risks and opportunities) first gained traction in 2017 in the context of the TCFD disclosure recommendations.

Today, it is embedded in major ESG disclosure frameworks, such as the CSRD with its ESRS standard for large companies in the European Union and climate-related disclosure requirements in the United Kingdom. The Japanese government has also been supporting TCFD-related disclosure by Japanese companies for several years.

The TCFD recommendations were also integrated into the reporting requirements under the ISSB standard, which has already led to the concept becoming more widespread in national legislation.

However, widespread adoption does not necessarily guarantee high quality. Investors need to be confident that companies are conducting scenario analysis robustly and comprehensively. Only then can the results be used to accurately assess companies’ vulnerability to physical climate risk.

For this reason, we examined the extent to which global companies’ disclosures indicate sound practices in climate scenario analysis. Our goal was to evaluate the initial phase of strategic management—namely, physical risk assessment—without extending into risk management, which we believe entails a distinct framework and warrants a separate, focused investigation.

Understanding Physical Climate Risks: Six Criteria For Robust Climate Scenario Analysis

We analyzed nearly 1900 global large and mid cap companies across 25 industry groups from the MSCI All Country World Index (MSCI ACWI), representing 85% of the index value.1

We screened over 4000 company reports from 2024— including annual, integrated, sustainability and TCFD/Climate reports— using a large language Model (LLM), looking for evidence for comprehensive climate scenario analysis aligned with the six criteria listed below. The criteria selection was informed by the disclosure requirements laid out in the European Sustainability Reporting Standards (ESRS), the TCFD’s guidance on scenario analysis and best-practice guidelines issued by the European Financial Reporting Advisory Group (EFRAG).

| The climate scenario analysis: | |

| 1 | considers a high warming scenario (or high water stress / high biodiversity loss scenario). |

| 2 | considers a longer term time horizon (5 years and beyond). |

| 3 | is based on scenarios by an authoritative organization such as the IPCC, IEA or NGFS. |

| 4 | considers both chronic and acute climate hazards. |

| 5 | results (qualitative or quantitative) about the company’s exposure are disclosed. |

| 6 | covers at minimum the company’s operations and key suppliers. For financial institutions, the analysis must cover customers (e.g., lending or mortgage book) or investments. |

We divided the company results into three categories:

| 🟢 | The disclosure meets all of the above criteria |

| 🟠 | The disclosure meets some (at least one) but not all criteria, and |

| 🔴 | The disclosure does not meet any criteria, meaning we did not find evidence that the company conducts climate scenario analysis for physical risk assessment. |

Global Climate Disclosures: Regional Gaps and Sector Blind Spots

Over three quarters (77%) of companies we analyzed met all or at least some of our criteria for comprehensive climate scenario analysis, suggesting that the use of scenarios for physical risk assessment has become a common practice. However, only 30% of companies meet all six criteria, highlighting significant room for improvement.

Across regions, European companies stood out, with 50% meeting all criteria, and the lowest proportion meeting none. This may be the direct result of stronger regulation, such as the CSRD, which came into effect this year.

By contrast, only 10% of North American companies provided comprehensive disclosure, potentially due to the absence of mandatory disclosure rules in the US. East Asia averaged 39%, but results varied widely with Japan at 51% and China at 19%.

Although some variations in disclosure practices were observed across prominent sectors, these deviations from the global average were often not significant. With the best performing sector achieving a share of 40%, there was no evidence to suggest that investors could reasonably expect comprehensive scenario analysis in any given sector.

Sectors with a relatively high proportion (>35%) of companies with complete disclosure included consumer durables & apparel, transportation, food & beverages, real estate and banks.

Whilst the deeper investigation of the drivers was outside the scope of this analysis, it could reasonably be assumed that in consumer durables & apparel and food & beverages, this behaviour is linked to strong supply chain dependencies on natural resources such as water and agricultural products.

In the real estate management and transport sectors, companies are highly dependent on the value and functionality of buildings and key infrastructure facilities, which makes physical climate risks particularly relevant and could motivate companies to measure and disclose risks. This pattern may not apply to real estate investment trusts (REITS), however, where the share of non-disclosers was relatively high.

In the banking sector, particularly in Europe, the climate stress tests repeatedly required by regulators and banks in recent years may have encouraged the wider adoption of scenario analysis practices and disclosures.

Sectors with a relatively low share (<25%) of companies meeting all criteria included healthcare equipment, financial services, energy and consumer staples.

The exact reasons for this may vary, from a lower perception of physical risks being financially material (health care equipment, consumer staples), to a generally lower level of transparency in climate-related disclosures (energy). Within financial services, excluding banks (e.g. asset managers, investment banks, brokers) practices appear to be less advanced than in banks, where climate stress testing has been enforced by regulators and supervisors.

Lastly, despite their reliance on freshwater for production, an above average share of companies in the semiconductor industry provided no evidence of conducting climate scenario analysis for physical risk assessment. This points to potential blind spots for investors in a sector that plays an important role in many investment portfolios.

Of those companies that only met some criteria for comprehensive climate scenario analysis, we also analyzed which criteria were most frequently met:

- We could not identify any significant deviations between the criteria. This means that no single criteria stood out as being frequently missed.

- However, we found that the consideration of long-term timeframes and both chronic and acute risks were the most frequently met criteria, showing that those criteria could be considered core criteria typically associated with physical risk analysis.

Finally, even in Europe, important gaps remain. Only 70% of companies explicitly stated that their physical risk assessments include suppliers. This suggests that, despite stronger overall disclosure practices, European firms often overlook the value chain more than companies in other regions. For investors, this gap underscores the need to scrutinize how thoroughly companies assess supply chain vulnerabilities, as unassessed risks could lead to unforeseen and significant disruptions.

Conclusions: What Physical Climate Risks Mean for Investors

Physical climate risks are an escalating concern that investors must both understand and integrate into their decision-making processes. Our research shows that global companies are increasingly adopting climate scenario analyses to evaluate these risks. However, the quality and comprehensiveness of these analyses vary significantly across regions, with European and Japanese companies setting the benchmark.

This regional leadership is likely driven by stringent disclosure regulations and governmental support for the Task Force on Climate-related Financial Disclosures (TCFD). These findings suggest that stronger disclosure requirements can significantly improve the quality of information available to investors, supporting better management of physical risks across diverse corporate portfolios.

Interestingly, our research did not reveal substantial variations across different sectors. Although sectors traditionally viewed as more vulnerable to physical climate risks—such as apparel, food and beverages, and real estate management—exhibit higher rates of comprehensive scenario analysis usage, no single sector emerged as a clear leader in widespread, high-quality application. This indicates the existence of numerous blind spots across all industries and underscores the need for meticulous, case-by-case analysis.

For investors, such in-depth analysis will be invaluable as physical climate risks continue to intensify globally. Companies with robust and forward-looking risk management strategies may secure a competitive edge in the future. Conducting thorough climate risk assessments is therefore a critical initial step toward achieving this advantage.

References

- Whilst all companies are theoretically exposed to physical climate risks, we excluded about 300 companies from sectors where we believe the risks to be less material. These were companies that are primarily service-based, very asset-light or with primarily digital business models.

Author Information