A Strategic Framework for Energy Security, Supply Chains and Geopolitical Risk

Ukraine was the lesson; Iran is the exam. The world has failed to study.

In February of 2022, following Russia’s invasion of Ukraine, mounting sanctions rendered Russian gas politically toxic. Prices soared, and household budgets tightened. Four years later, following US-Israeli strikes, Iran’s Revolutionary Guard broadcast a decisive warning over maritime radio: no ship would be permitted to pass the Strait of Hormuz, one of the world’s most critical shipping corridors. Predictable outcomes followed: spiking prices and acute economic uncertainty.

Today, it is Ukraine and the Gulf. Tomorrow, it could be China and Taiwan, and with it, 92% of the world’s advanced semiconductors. This pattern is no longer a mere warning. It is a standing vulnerability that demands structural resilience. Structural resilience requires a structural framework. ESG, reimagined as Energy, Sovereignty, Geostrategy, provides exactly that: the deliberate use of infrastructure, resource autonomy, and supply-chain redesign to reduce geopolitical exposure. In this framing, sustainability is not a moral framework for environmental or social virtue. It is the strategic architecture of national resilience.

From Ukraine to Hormuz: What Energy Crises Reveal about Global Vulnerability

Following Russia’s invasion of Ukraine, Europe cut its dependency on Russian gas from pre-invasion levels of 45% to 13% by 2025; dependency on Russian oil followed a similar trajectory. As great a triumph as it was to reduce Russian dependency and Putin’s coercive leverage, the internalization of a more general lesson concerning the dangers of resource dependency would have been an even greater achievement for European autonomy. Sadly,this broader lesson failed to materialize.

Europe replaced Russian pipeline gas with seaborne liquefied natural gas (LNG) from the US. Unfortunately, that did not insulate the bloc from the crisis in the Strait of Hormuz. When roughly 20% of supply effectively disappears from global markets, spot prices spike irrespective of where your cargo was loaded. European natural gas prices nearly doubled during the escalation of the Iran conflict.

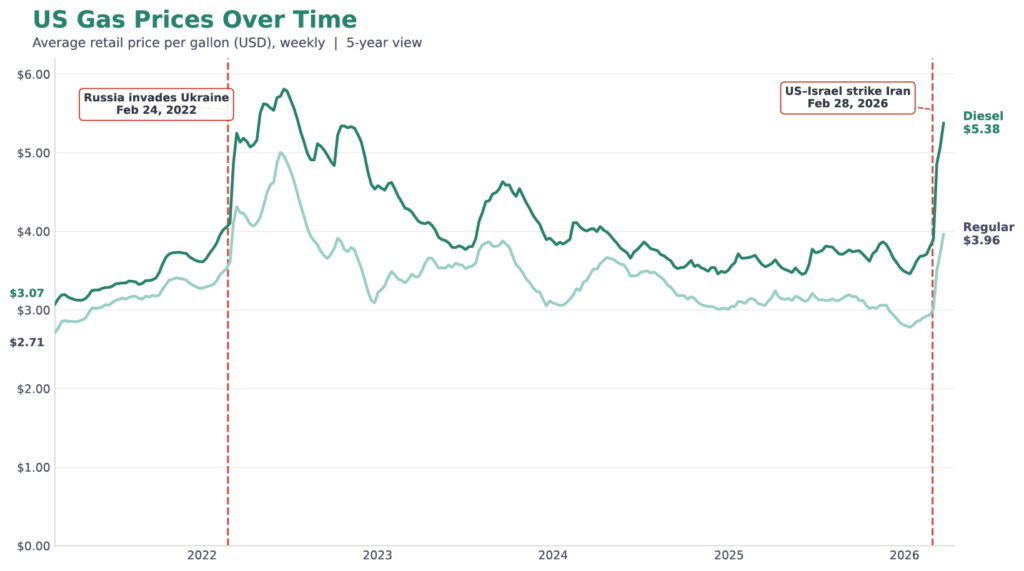

Even the US, which has long pursued the political objective of energy independence, was vulnerable to the same fate. In practice, most of the gasoline and diesel that US consumers pump into their vehicles is refined from imported oil, leaving the US subject to the same market dynamics as Europe. Consequently, diesel prices surged by 34% in the US, while gasoline prices jumped to their highest levels since October 2023. Indeed, five-year highs in both gasoline and diesel came in the days, weeks, and months following Russia’s invasion of Ukraine.

Figure: US gasoline prices over a five-year horizon

History offers us copious lessons from which to learn, but it rarely offers them in such brutally rapid succession. Substituting suppliers is not sovereignty. Such actions may reduce discrete dependencies, but they do not exorcise systemic vulnerabilities. Sovereignty begins only when a nation can meaningfully reduce its external exposure in the first place.

Beyond Oil: How Supply Chains and Critical Resources Become Strategic Risks

The first instinct is to read the closure of the Strait of Hormuz solely as an energy crisis. It is much more. The Strait is a single chokepoint with multiple cascading consequences; a classic example of systems failure.

For example, one-third of all global fertilizer trade moves through the Strait. When the waterway closed, urea (a critical fertilizer) prices at the New Orleans port rose more than 25%. This led the President of the American Farm Bureau to write a letter to US President Trump, warning that shortages of both fuel and fertilizer represented a threat to US food security, affordability, and national security.

Now, just at the start of planting season, far beyond the Great Plains of the US, farmers around the world are keeping a uniquely keen eye on the headlines, not because they have a passion for international political economy but rather because a chokepoint that they never think about is now deciding what they can afford to grow and what the rest of us can afford to eat.

As we look to potential conflicts of tomorrow, energy and food are only two threads of a much more complex tapestry. China, for example, accounts for 91% of rare mineral refinement processes. Meanwhile, Taiwan is responsible for more than 60% of global foundry revenue and 90% of leading-edge chips. The pattern continues: critical resources fundamental to the modern economy are concentrated in contested geographies in which countries cannot exert control, with no near-term substitutes.

This is the topography of modern risk.

A New ESG Framework: Energy Security, Sovereignty and Geopolitics

In response to these risks, ESG should no longer be primarily treated as a disclosure regime or a reputational exercise. Rather, its strategic value lies in helping nations and companies to identify and reduce exposure to external leverage over the resources on which economies depend.

Energy sovereignty is the first and most salient domain. Here, the renewable energy debate has been misclassified for a generation. Yes, emissions matter, but the more urgent question concerns whether a nation’s economy can be held hostage by events it does not control, in places it cannot secure. Ukraine and Iran are not anomalies. They are the recurring costs of systems built on geopolitical fault lines.

Spain makes the case concretely. Following aggressive expansion of wind and solar post-2019, Spanish industrial electricity costs are 32% below the EU average. Instructively, national electricity prices have risen very modestly relative to peers since the outbreak of the Iran conflict. In effect, Spain has built structural grid insulation and, with it, a degree of geopolitical independence that its more fossil fuel-dependent neighbors now visibly lack.

The same logic extends beyond energy. Domestic fertilizer production and diversified agricultural supply chains are not environmental aspirations. They are a food security infrastructure. Indeed, the US now formally classifies critical components like phosphate and potash as critical materials under the National Farm Security Action Plan. The US Department of Agriculture’s own language is unambiguous: dependence on foreign sources for critical agricultural inputs “can threaten [US] domestic security and independence”.

Similarly, investment in circular economies and critical mineral recycling is not a concession to environmentalists. It is an industrial strategy for a world in which supply routes cannot be guaranteed. The EU has already codified this logic. In 2024, the European Commission approved the Critical Raw Materials Act, targeting domestic extraction, processing, and recycling of materials essential to defense, energy, and advanced manufacturing. The EU’s explicitly stated objective is one of security: reducing dependence on concentrated supply chains that can be leveraged against it. The US has taken similar steps, announcing plans for critical mineral stockpiling, focused domestic investment, and international coalitions to avoid overdependence on potentially adversarial nations.

The Next Decade: Energy, Supply Chains and the New Architecture of Systemic Risks

The lesson bears repeating: Ukraine and Iran have underscored that independence is not achieved by diversifying suppliers, but by eliminating the dependency itself.

A nation is not sovereign if it can be destabilized by a pipeline cut abroad, a strait closure thousands of miles away, or a mineral embargo imposed by a geopolitical rival. A company is not resilient if its core inputs depend on routes, jurisdictions, or suppliers that can be disrupted overnight. An economy is not secure if critical resources remain concentrated in contested geographies with no viable alternatives at scale.

That reality demands a new reading of ESG as a framework for reducing structural dependence, increasing national and industrial resilience, and preparing economies for a world in which geopolitical shocks are no longer exceptions, but conditions. The new ESG is Energy, Sovereignty, Geostrategy.

The data exists. The frameworks exist. The question is whether the will to act on them can survive the complacency between one crisis and the next.

Author Information