Translation powered by AI which may cause imperfections

Introduction

Across the globe, consensus is growing as to the urgent need to transition to a more sustainable economy. As a result, governments and regulators have been busy designing their respective regulatory regimes to ensure that capital can flow efficiently to sustainable companies and projects. A key objective in all of these regulations is the need to limit greenwashing, where environmental or social characteristics are exaggerated. That objective is extremely complex and the essential elements to ensure compliance are still elusive. Another challenge relates to ensuring some commonality in the understanding of the same terms between industry, regulators and investors and across borders. For instance, can investors understand the difference between risk and impact, and do we have a common definition of what different ESG terms mean, and what it means to be sustainable?

Previously, much of the regulatory action was focused within the European Union. Lately, however, we are seeing an increase in activity outside the EU. In this paper, we compare three prominent regulatory proposals for investment funds in the EU, UK and US. We find limited alignment between the differing regimes. This lack of alignment between the three jurisdictions could lead to difficulties for asset managers and fund distributors who are attempting to market the same ESG fund across different jurisdictions. This may mean that the level of sustainability of a given financial product may depend more on where it is located, than its characteristics. Therefore, rather than focusing their attention on creating sustainable products that reflect consumer demand, many financial market participants may spend more time and money tweaking the name or asset structure of their funds depending on their regulatory jurisdiction. In practice that limited regulatory alignment is encouraging these issuers to create sub-optimal products just to meet various geographical standards, resulting in a poor outcome for investors, markets and the transition to a sustainable economy.

Three Regimes

To understand the challenges across jurisdictions we must first understand the nuances of each geography’s regulatory regimes. Below you will find a summary of the three proposals:

EU

Categories (not labels)

Article 6

Article 8: promote E/S characteristics

Article 9: sustainable investment objective

Naming rules

Proposed rule for use of ESG terms or sustainability derived term in name:

- Any ESG term: 80% of the assets it invests in should be used to meet the ESG-related characteristics that it promotes (i.e. aligned with the terms in the name).

- Sustainable or derived term: minimum 50% invested in sustainable investment (SI) as defined by Article 2 (17).

Minimum Threshold of Sustainable Investment (SI, or similar)

Under SFDR: Article 9 funds should only make Sustainable Investments (i.e. close to 100%) Under ESMA’s recent proposal: 50% minimum SI if name uses word “sustainable”.

Share of investments aligned with fund name

Per the naming rule, Article 8 with ESG-term in fund name: 80%.

UK

Labels

ESG Focus

ESG Impact

ESG Improver

Naming rules

- Under the general naming and marketing rule: restrict the use of certain sustainability-related terms for products that do not use one of the above labels.

Minimum Threshold of Sustainable Investment (SI, or similar)

If using ESG Focus label: 70% of assets to be invested to “credible standard of sustainability”.

Share of investments aligned with fund name

If using ESG Focus label, 70% aligned to environmental or social theme.

US

Labels

ESG Integration

ESG Focused

ESG Impact

Naming rules

Under the proposed amendments to the “Name Rule”: any fund name which suggests a focus on ESG terms must invest at least 80% of their assets aligning with that ESG focus.

Minimum Threshold of Sustainable Investment (SI, or similar)

No equivalent in current proposed SEC rules.

Share of investments aligned with fund name

Per the name rule, 80% of assets aligned with strategy that name suggests.

European Union

The Sustainable Finance Disclosure Regulation (SFDR) is the EU’s flagship disclosure regulation for investment funds. The Level 2 regulatory technical standards (RTS) have been in force since January 2023, though the main provisions of the regulation have been operational since March 2021. In April 2023, the European Supervisory Authorities (ESAs) launched a review of the RTS.

A key concept within SFDR is that it represents a disclosure system for funds, rather than a fund labeling regime. Nevertheless, there are three categories of funds within the SFDR and much of the market has been using those classifications as de facto labels:

- Article 6 funds: Have no sustainability related objectives but must still make disclosures including how they incorporate sustainability related risks into their investment decision making.

- Article 8 funds: Make investments to promote sustainability related characteristics.

- Article 9 funds: Have sustainability related investments as their primary objective.

In terms of minimum standards, the regulation stipulates that Article 9 funds should invest only in “sustainable investments”. Though the regulation does not stipulate a figure, we would expect Article 9 funds to invest close to 100% in sustainable investment and for the purposes of the analysis within this paper have used a minimum sustainable investment and “allowing for cash and hedging” would expect a minimum sustainable threshold of 80 to 90%. For the purposes of the analysis in this paper, we have used the more conservative 90% figure. No equivalent advice for minimum threshold currently exists for Article 8 funds.

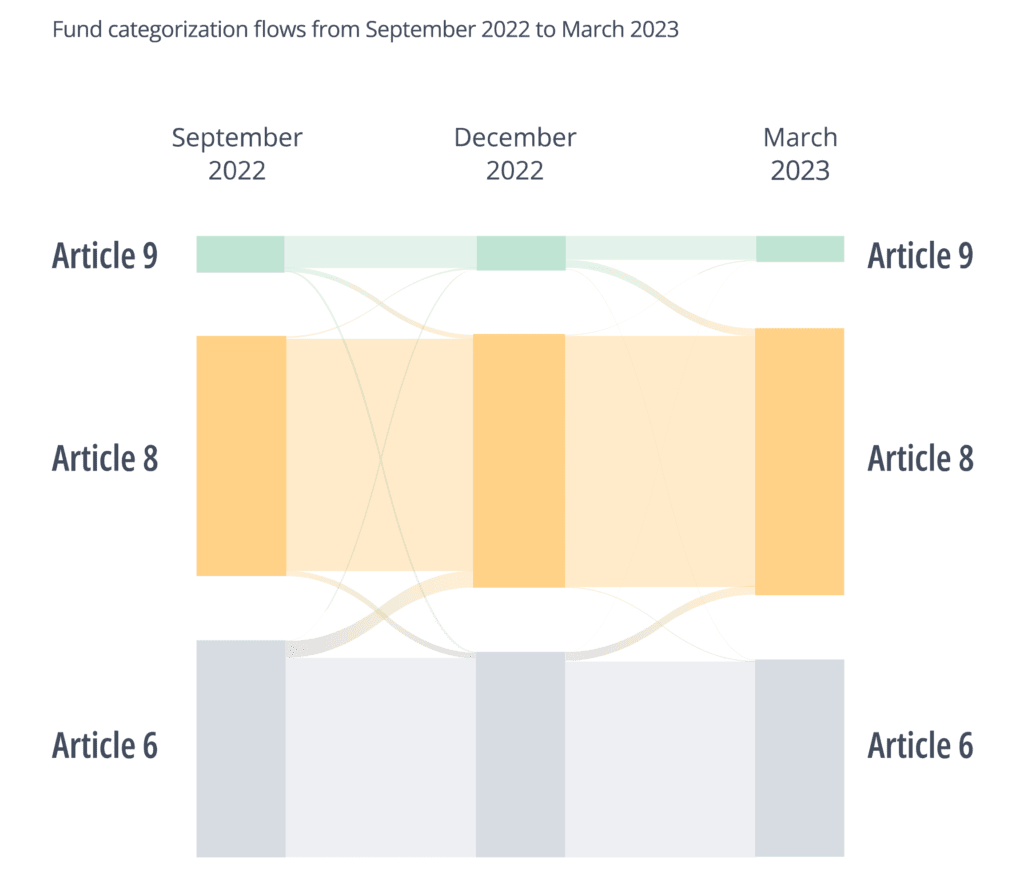

According to reports, end investors are increasingly demanding Article 8 and 9 funds meaning that Article 6 funds are becoming more and more difficult to market. A combination of this, and the high bar for Article 9 funds, has turned Article 8 into a “catch all” category, encompassing a broad array of funds with wildly different sustainability characteristics.

Recently, we have seen an increase in funds “upgrading” from Article 6 to Article 8. In the run up to the Level 2 RTS that came into force in January 2023, we also saw a trend of fund “downgrades” where Article 9 funds reclassified themselves as Article 8 funds. Our hypothesis for those downgrades is that funds were uncertain about the regulatory requirements to be considered Article 9 and – in the face of uncertainty – preferred to take a cautious approach. This bolstered the idea that Article 8 was becoming a “catch all” category. These movements can be seen in the below chart.

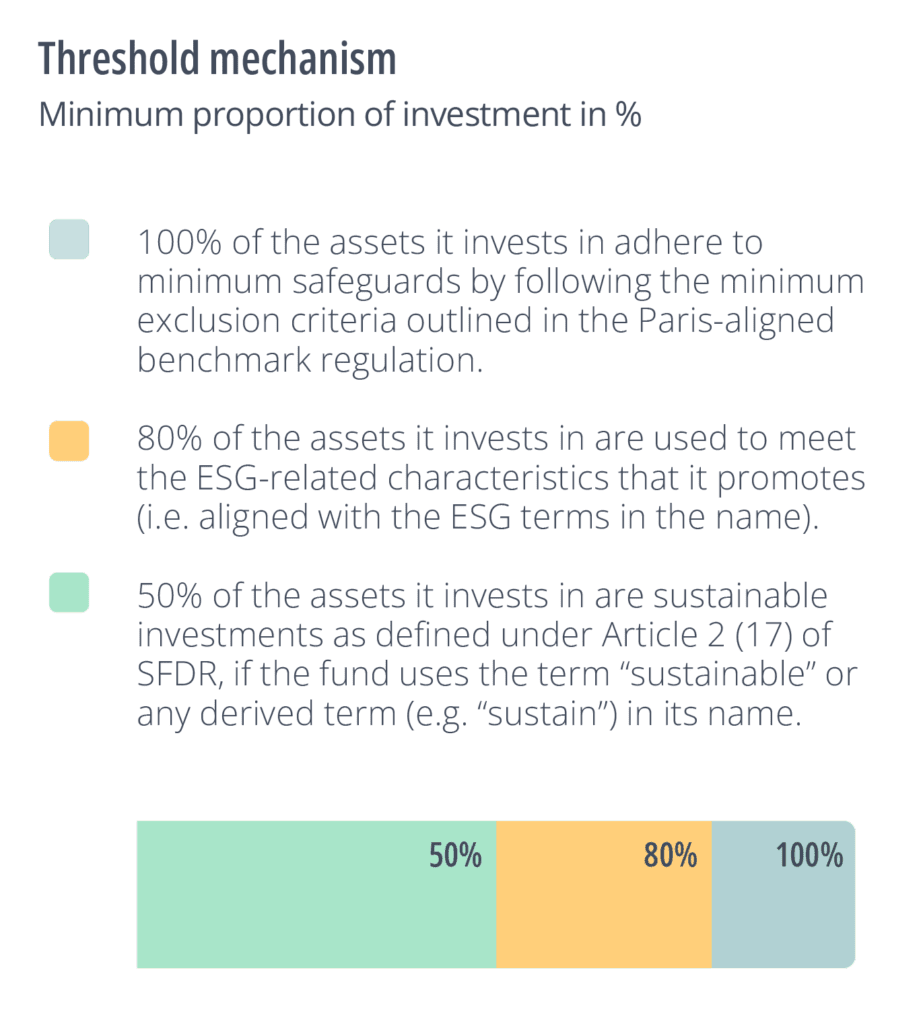

As a response to the uncertainty, ESMA released a consultation in November 2022 which sought to put more rigor behind the Article 8 funds that used certain ESG terms in their names. For Article 8 funds they proposed:

- 100% of the assets it invests in adhere to minimum safeguards by following the minimum exclusion criteria outlined in the Paris-aligned benchmark regulation.

- 80% of the assets it invests in are used to meet the ESG-related characteristics that it promotes (i.e. aligned with the terms in the name).

- 50% of the assets it invests in are sustainable investments as defined under Article 2 (17) of SFDR, if the fund uses the term “sustainable” or any derived term (e.g. “sustain”) in its name.

For more information on this proposal, refer to “A Glimpse Into the Future”, found later in this paper.

United Kingdom

Sustainability Disclosure Requirements

In October 2022, the FCA published its Sustainable Disclosure Requirements (SDR) consultation paper (CP). SDR will mandate the disclosures that different sustainable funds need to make in the UK, and outlines three labels to represent different types of sustainability strategies: ESG Focus, ESG Improvers and ESG Impact. The finalized rules were recently delayed and are now set to be delivered in Q3 2023.

The three labels are a change from earlier expectation that the regulation would stipulate five categories, with the FCA opting for a more simplified approach. The FCA has stressed that the labels are not hierarchical and instead indicate the objective of the fund:

- Focus: This label suggests that the fund maintains a high standard of sustainability in the profile of the assets (fund should invest at least 70% in sustainable assets suggested in the CP). At present there is no suggestion to include a “Do No Significant Harm” concept within the FCA’s concept of sustainable investment. For the purposes of our analysis below, we removed the DNSH condition from our SI model.

- Improvers: This label is the most novel and indicates that the product invests in assets that may not be sustainable at present but that have committed to improvements or are in transition to becoming more sustainable. Key to this category is the idea of “stewardship” on the part of the asset manager to make a “measurable” improvement in underlying ESG performance.

- Impact: These are products with a specific sustainable outcome as an objective (to “achieve a pre-defined, positive and measurable environmental and/or social impact”), with no minimum level of sustainable investment required.

- Other: Funds that do not meet the criteria for a sustainable label.

Similar to SFDR, disclosures will be split between pre-contractual, and then ongoing product and entity level sustainability reports. The pre-contractual materials will include information on the sustainability objective and investment strategy. The product report will include TCFD information and sustainability performance metrics, though is unlikely to mirror the Principal Adverse Impact metrics (PAI) that form a core part of the SFDR. Alongside the fund labels, the FCA is introducing rules around naming and marketing of funds. The FCA is suggesting to prohibit the use of any sustainability related term in the naming or marketing of funds, unless that fund uses one of the three labels set out above. The FCA does not provide a comprehensive list of captured terms but does mention: “ESG”, “environmental”, “social”, “governance”, “climate”, “impact”, “sustainable”, “sustainability”, “responsible”, “green”, “SDG”, “Paris-aligned” or “net zero”. For the Focus and Improver categories, it is also prohibited to use the term “impact”.

United States

Fund disclosures

The SEC also recently proposed rules in the form of amendments to the Investment Company Act of 1940. The amendments will require asset managers to disclose additional information pertaining to their ESG investment practices and the SEC is proposing three different categories of funds to reflect different types of sustainability related objectives. These requirements, which are to be finalized by October 2023, aim to provide consistent information on strategy and ESG investments for end investors. The proposed amendments only apply to those who use an ESG label or consider ESG factors in their investment process. Funds who do not incorporate ESG factors are not mandated to do so under the proposed amendments.

Proposed amendments

The proposal identifies three types of ESG funds:

1. Integration Funds

Description: Funds which integrate both ESG and non-ESG factors in investment decisions.

Disclosure: Explanation of how ESG factors were included in their strategy.

2. ESG-Focused Funds

Description: Funds which give significant importance to ESG factors in investment decisions (e.g. through inclusionary or exclusionary screens, engagement with issuers and/or seeking a specific impact).

Disclosure:

- Detailed disclosure about their strategy, including a standardized ESG strategy overview table or template.11 • Proxy voting or engagement with issuers as part of ESG strategy must be disclosed.

- Portfolio’s carbon footprint and weighted average carbon intensity.

- Use of exclusionary screening methods, if applicable.

- How they consider GHG emissions, including the methodology and data sources used.

2.1 Impact Funds

Description: Funds which are ESG focused seeking to achieve a particular ESG impact (a subset of “Focus” above).

Disclosure: Same template as Focus funds. Qualitative and quantitative measures of progress in achieving its ESG objective.

Name Rule for Funds

In May 2022, the SEC also proposed amendments to the Investment Company Act Names Rule, in order to prevent fund names from misleading investors about a fund’s investments and risks. These rules are aimed at investment funds using ESG terms in their names and are to be finalized by October 2023.

Proposed amendments

The proposed amendment to the Names Rule expands the scope of the 80% investment policy requirement to any fund name which suggests a focus on any specific characteristics to cover ESG terms. The rule prohibits funds from using ESG or similar terminology in their name if ESG factors are not centrally considered in investment decisions. This means that funds using ESG or similar terminology would be required to invest at least 80% of their assets aligning with an ESG focus.

Some Key Differences

- European regulations to date tend to distinguish less between different types of sustainability objectives being pursued by the financial product. For instance, Article 8 or 9 do not mention whether the fund is focused on improvement, transition, impact or sustainable focus. Both the US and UK regimes try to do this through use of different labels.

- In relation to disclosures, the US Integration label could be considered as similar to Article 6 funds, which still need to make certain disclosure about how they integrate ESG risks into their investment policy.

- The criteria underpinning the UK and US labels are different. (e.g. for UK Focus, need 70% assets to be invested to credible standard of sustainability (further clarity was not provided in the FCA consultation)).

- In Europe, Article 9 requires close to 100% of its assets to be sustainable (under article 2 (17), and the recent proposal by ESMA suggests that Article 8 funds with “sustainable” in their names should invest 50% in sustainable investment).

- For naming rules, the UK excludes use of ESG terms unless one of the three labels is being used. US and EU (proposals) both have 80% minimum of assets that need to be aligned with the naming of the fund where ESG terms are used.

Regulatory Case Study

A Glimpse into the Future: Using the ESMA Consultation as a Case Study for Future Regulatory Developments

The European Union remains the leader in sustainability regulations so while other jurisdictions are shaping their regulatory regimes we examined ESMA’s latest consultation as a case study and possible precursor for those regulations still taking shape elsewhere.

Unfortunately, it seems that although ESMA set out to clarify fund names, the changes coming out of the proposal may not significantly reduce the amount of confusion in the market.

In order not to mislead investors, ESMA believes that ESG- and sustainability-related terms in Article 8 funds’ names should be supported in a material way by evidence of sustainability characteristics or objectives that are reflected fairly and consistently in the fund’s investment objectives and policy.

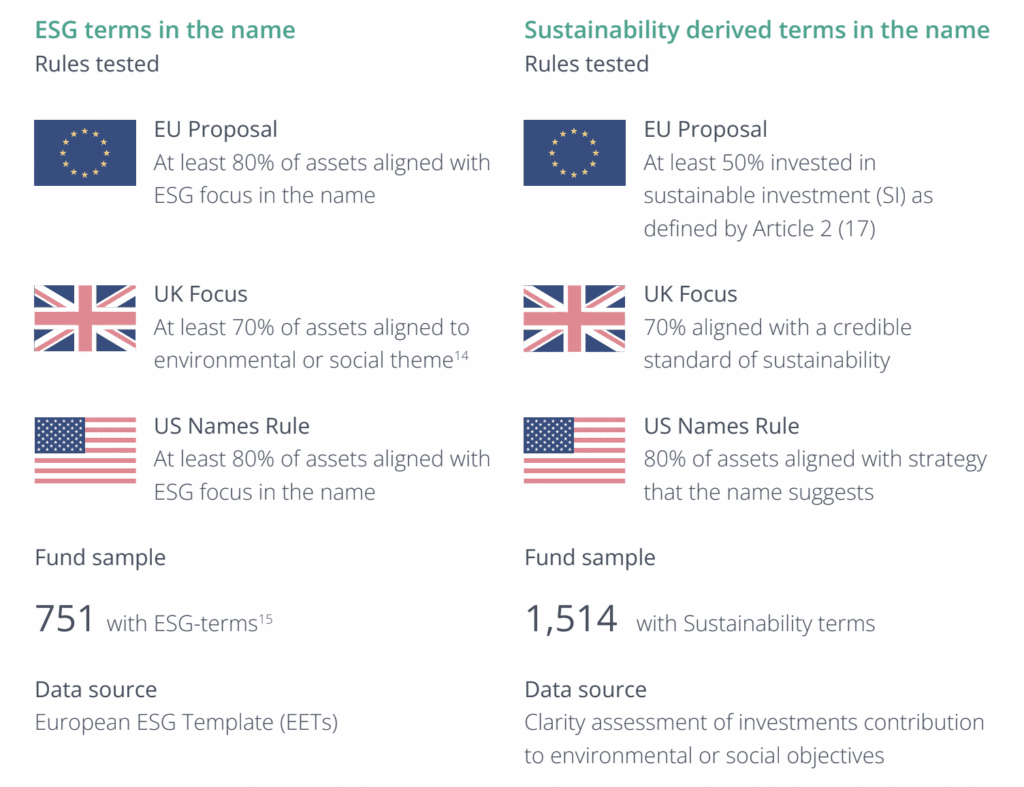

Therefore, in November 2022, ESMA released a consultation that sought to put minimum thresholds in place for Article 8 funds that use certain ESG or sustainability-related terms in their names. See Figure 2.

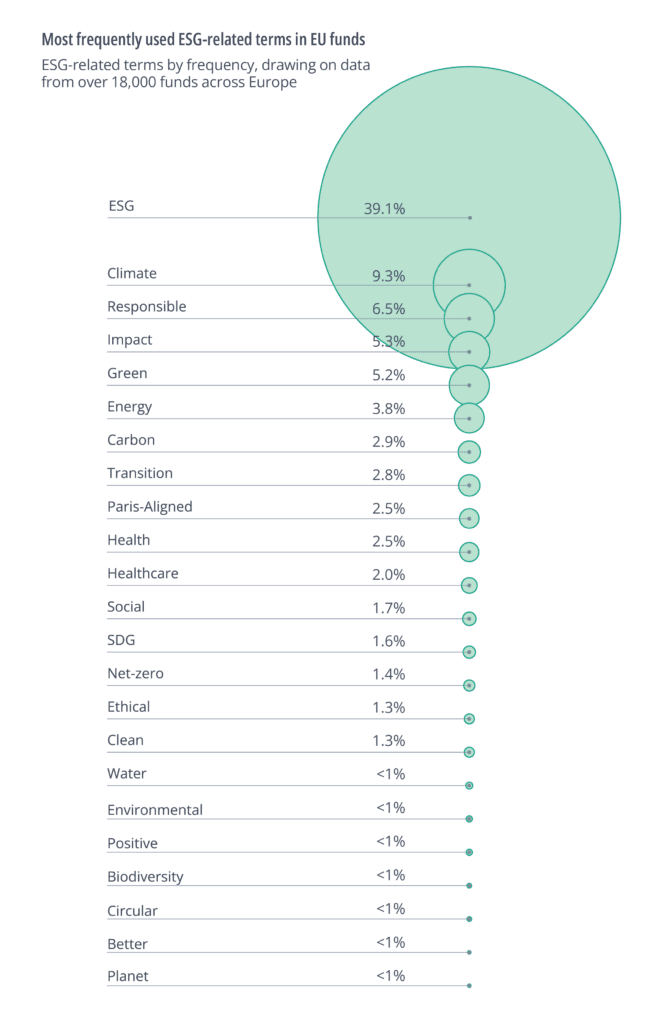

Clarity AI examined these proposals, drawing on data from over 18,000 funds across Europe.12 For ESG related terms, little guidance was offered by ESMA on those terms in scope of the proposal. We therefore used the terms that appeared most frequently in fund names, as outlined in Figure 3.

We also examined funds containing the term “sustainable” or any term “derived” from that word: “sustainable”, “sust”, “sustainability”, “sus”, “sustnby”, “sustain”, “sstby”, “sstnb”.

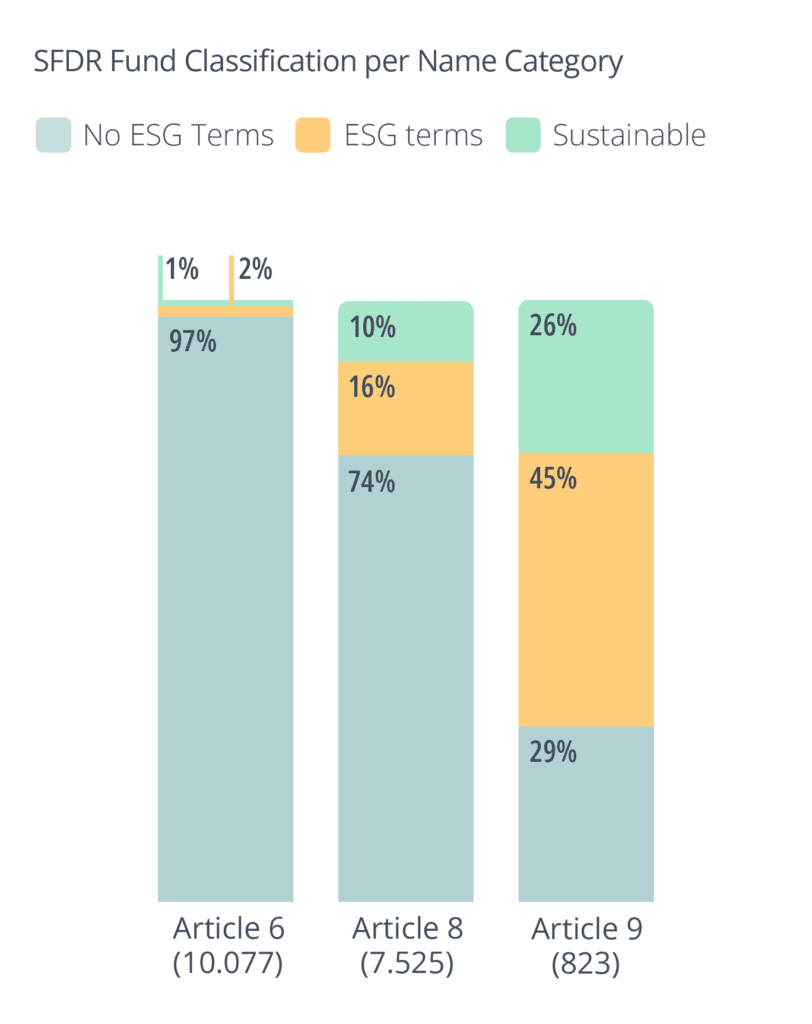

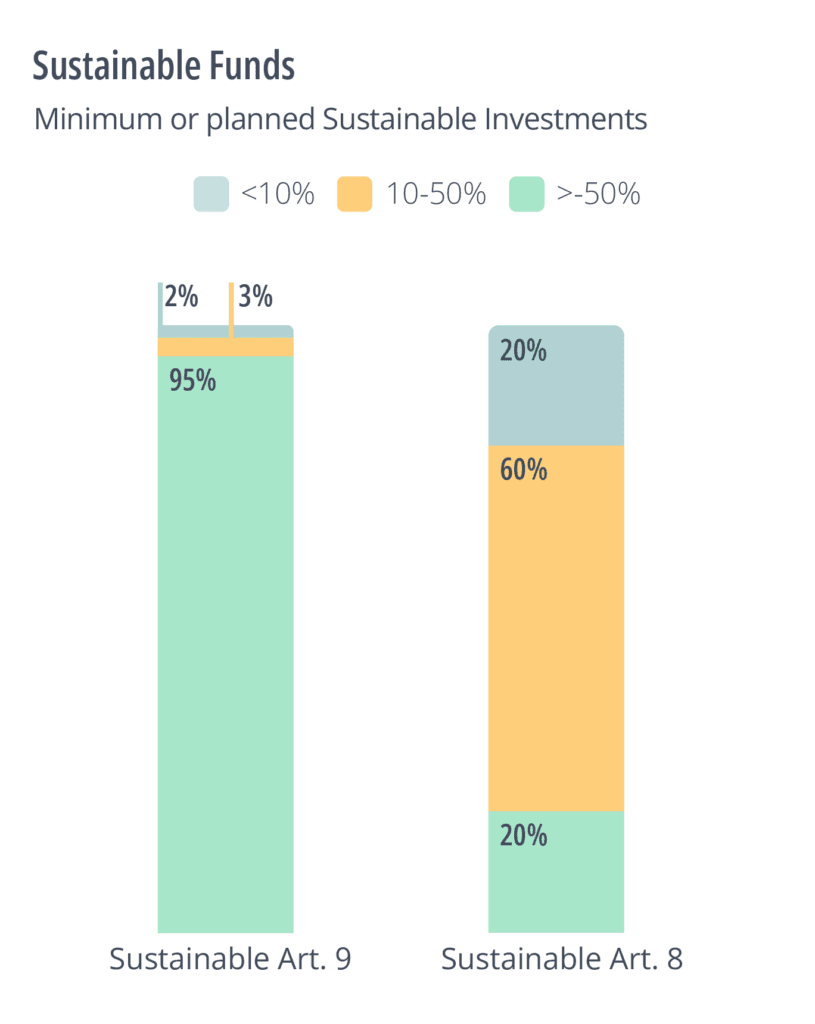

This result adds weight to the argument that Article 8 has been used as a catch all category. Nearly three quarters of the Article 8 funds in our universe made no reference to ESG (including sustainability) in their name. This also suggests that ESMA’s proposal will have a small impact on the market. As can be seen below, Article 8 funds also on average have low levels of sustainable investment as defined by Article 2 (17) of SFDR.

To test the ESMA proposals on the funds that do have references to sustainability, we looked at the planned (via EETs) and actual (via Clarity AI’s own data) level of sustainable investment in different Article 8 funds. We found only 20% of Article 8 funds with the term sustainable (or a derivative thereof) currently plan to make sustainable investment of over 50% as outlined by the consultation. These funds would therefore fall short of the terms of sustainable investment made by Article 8 funds with “sustainable” in their names: a similar number (20%) plan to make less than 10% sustainable investment. Similar results were found using Clarity AI’s own data.

What Does the Data Tell Us

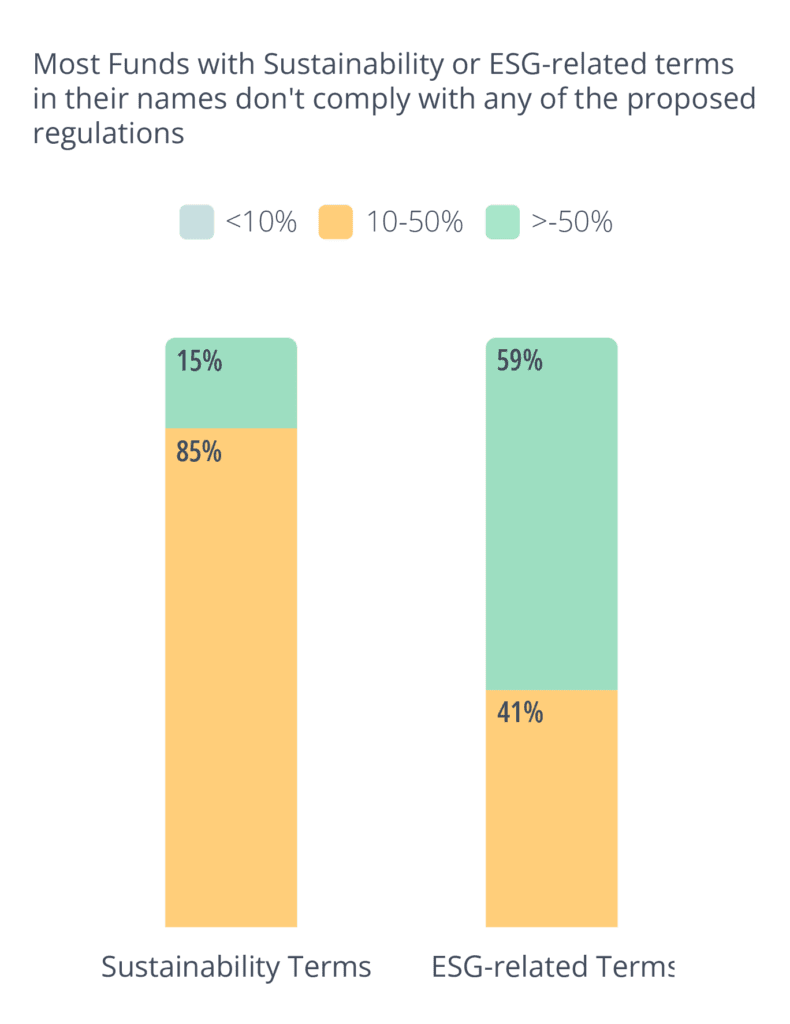

While much has been said about the theoretical differences between the three regimes we wanted to quantify whether that really made a difference for funds that are currently being marketed as sustainable. We find two interesting results that will have implications for fund managers as the proposed regulations come into play:

- Most funds with sustainability or ESG terms in their names currently do not comply with any of the proposed naming rules in the regulations.

- The heterogeneity of the regulations means that a high share of funds with Sustainability terms in their names will not be able to market themselves in a consistent manner across the three markets, but funds with ESG-terms in their names will not face the same problems.

Given the EU differentiation of funds with Sustainability and ESG terms in the name our analysis focused on two groups of funds and used different data sources as summarized in the table below:

In order to calculate the proportion of investments aligned with the name for funds with ESG related terms, we relied on the data self-reported by these funds in the EETs. This analysis therefore focuses on EU funds, whereas the analysis using Clarity’s SI definition can examine funds from UK and US as well as EU.

In the case of funds with sustainability related terms in the name, we relied on Clarity AI data and research that assesses whether companies are aligned with the EU Taxonomy, SDG framework, or are best performers in terms of the Principal Adverse Impact indicators most relevant for them. For the EU proposed regulation we also considered the DNSH and good governance criteria, which are part of the definition of Sustainable Investment included in this regulation.

The conclusions of this analysis showed that overall, a small share of funds meet any of the requirements for the different labels or categories under the regulatory frameworks with at least one of the three proposals. In other words the majority of the funds are unlikely to comply with any of the proposals. Specifically, only 15% of funds with “Sustainability” in their name and 59% of funds with ESG-related terms have been found to meet the criteria under the proposed regulatory frameworks with at least one of the proposed regulations.

As these regulations come into play, fund managers will need to adjust their strategies in order to continue positioning their funds as sustainable.

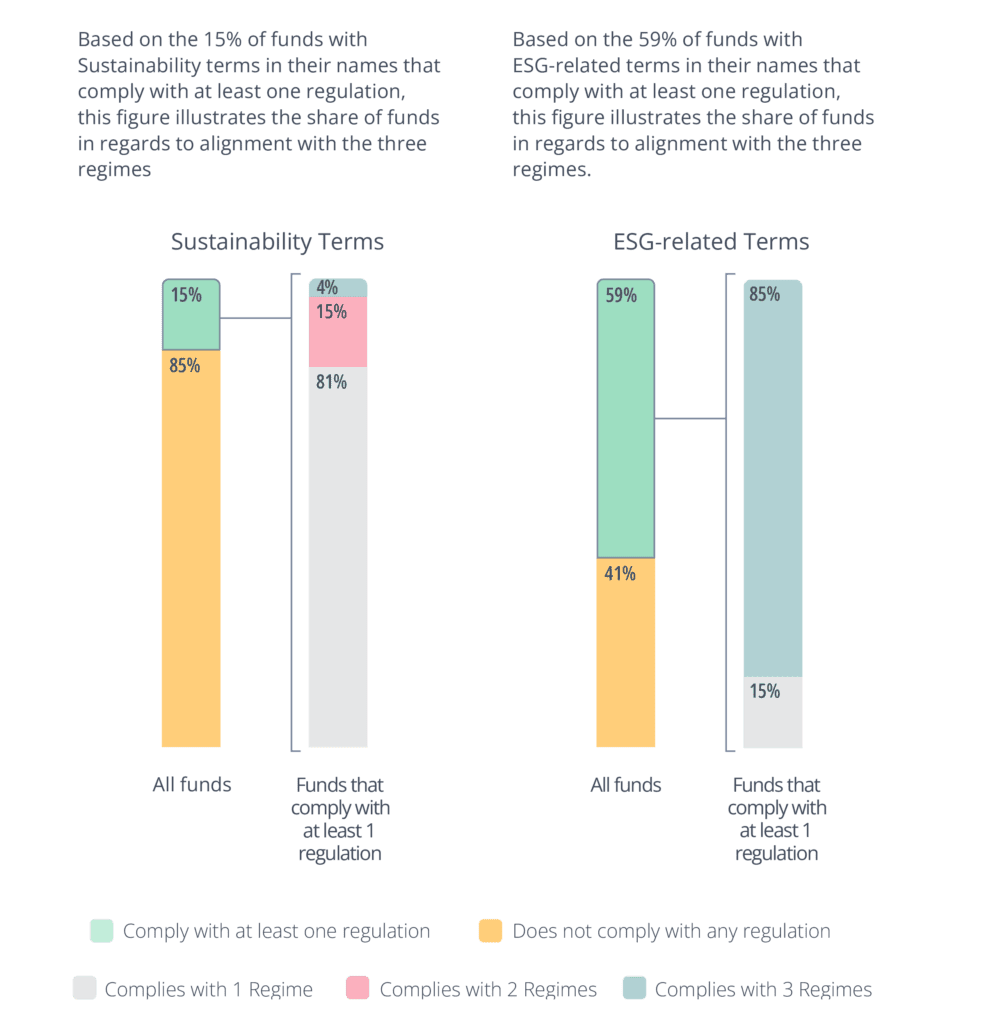

To quantify the differences between the three regimes we looked closer at the 15% and 59% of Figure 6 that comply with at least one regulation. For that sub-sample we calculated the share of funds that would satisfy the conditions proposed by one, two or all three of the regimes (Figure 7 and 8).

Our analysis revealed that the regulatory regimes differ significantly in their requirements for funds with “Sustainability” in their name. Specifically, 81% of funds would only comply with one of the regimes, and only 4% of funds would comply with all three. In other words, over 95% of funds would require renaming or restructuring to sell across all three markets.

In contrast, the requirements for funds with ESG-related terms in their name were more consistent, with 85% of funds complying with all three regimes. This discrepancy could incentivize fund managers to prioritize creating funds with ESG-related terms in their names that can be sold in different markets, rather than adjusting their strategies to meet the criteria for funds with “Sustainability” in their name.

Case Study

To illustrate the difficulty of marketing the same fund in the same way across the three geogra phies, we analyzed some stylised examples of funds. We sought to examine funds that mimicked real examples examined them through the lens of each regulatory authority.

The examples are inspired by examples provided within the ESMA proposal, SDR consultation, and SEC proposed rule.

Example 1: Sustainable Waste and Water Fund

This is an actively managed fund focused on waste and water. It invests 70% of its assets are involved in the manufacture or sale of products used in connection with waste and water management. This suggests a connection to, amongst others, Goal 6 of the UN Sustainable Development Goals (clean water and sanitation). As it meets the 70% threshold, it would be able to use the FCA ESG Focus label.

This fund manager may encounter difficulties in marketing the same fund in Europe (under ESMA’s proposed rules) and the US (under the Names rule). Because it uses the term “sustainable” it would need to demonstrate that 50% of its assets are sustainable investments under Article 2 (17). According to its SFDR disclosure, the fund only plans to make 35% sustainable investment. Given it uses an ESG-term (“water”, “waste”), it would also need to demonstrate that 80% of its assets are used to promote the environmental or social characteristics it promotes (at present it appears that number is 70%).

Similarly, it would struggle to sell in the US where a similar 80% threshold would apply to ensure the investments were aligned with the focus the fund’s name suggests.

This fund may decide to alter its asset structure to enable it to market itself across all three jurisdictions with minimal friction. This may lead to the fund becoming more focused in its sustainability related goals. However, it may also lead to investment in assets that are less related to its objective in order to inflate its sustainability profile. This fund would also need to consider whether it could change its name to help it move more freely between regulatory regimes.

Removing the term “sustainable” would relax the minimum sustainable investment percentage in Europe. Alternatively, removing the terms water and waste may make it easier to market in Europe (though not necessarily in the US unless the term sustainable was also removed). In any event, such tweaks to the name do not appear to enhance the sustainability of the underlying assets or the ease with which retail investors can understand the purpose of the fund. We therefore see this as a sub optimal outcome.

Example 2: Global Impact Fund

This example is an EU fund that invests 85% of its assets in equity securities that address global social and environmental issues. It plans to invest 85% of its assets in sustainable investments as defined by Article 2 (17). ESMA’s proposal regulates the term “impact” by stipulating that funds using “impact” or related terms should meet the proposed thresholds of other ESG terms and “additionally make investments with the intention to generate positive and measurable social or environmental impact..”. Under the ESMA proposal therefore, this fund would make the threshold of an Article 8 fund using ESG terms.

Under the FCA’s SDR proposal, “impact” is defined as a fund that achieves “…positive, real-world impact” by solving environmental or social problems. Central to the FCA’s impact definition is the concept of “additionality”, whereby fund managers will have to prove some “extra good” has taken place as a direct result of their investment (i.e. in the counterfactual, if their investment had not taken place, the impact would not have happened). This sets a high bar, and in particular with publicly listed companies it might be very difficult to demonstrate such additionality. It is therefore unlikely that this fund would be able to read across directly to the FCA’s ESG Impact proposed criteria.

The SEC proposed rule defines impact as any fund having a “stated goal that seeks to achieve a specific ESG impact… that generate specific ESG-related benefits.”

Under the proposal, the impact fund would need to detail the specific impact it intends to have with additional disclosures required

on an ongoing basis to demonstrate “how the fund measures progress towards the stated impact; the time horizon used to measure that progress; and the relationship between the impact the fund is seeking to achieve and the fund’s financial returns.” While this definition appears to be closer to that of the EU, it is clear that across the jurisdictions there are three differing understandings of the same term.

It is possible therefore that asset managers might avoid impact-based strategies and pare back their sustainability ambition to ensure an easier path across the three jurisdictions. This represents a sub optimal outcome to the extent end-investors demand impact-based strategies.

Conclusion

Different regulatory jurisdictions may have good reasons to build their regulatory regimes in different ways. For instance, market dynamics may have important nuances across borders and the political environment in which the rulemaking happens can have significant impact on how final rules look. Nevertheless, there are considerable benefits to cross border regulatory alignment. This is particularly true in financial markets that are inherently international and rarely respect geographic borders.

We see this come to life in our analysis, with 85% of funds with sustainability related terms in their name not meeting regulatory requirements. Of the funds that do comply, only 4% would comply across all three regimes, which leaves both issuers and investors even more confused than before the regulations were enacted.

Although we do not think it is realistic to advocate for total coordination across borders, we would push for as much regulatory alignment as possible, which should provide better outcomes for all participants. In this sense, international organizations such as the International Organization for Securities Commissions and the International Sustainability Standards Board could be important for ensuring a common baseline across borders.

In this paper, we have presented the three different approaches to regulating sustainability disclosures and labels of investment funds. The intention of these regulations were simple, to reduce greenwashing and increase capital flows, but with such disparity across regulations and even within each regulation what we are left with is an environment of confusion, which is fraught for perversion.

Clarity AI seeks to tackle this confusion with an unbiased view of a portfolio’s sustainability. Investors need to understand how their investments fit across the various regulations and they need transparent and granular data to uncover what is behind the labels. Leveraging advanced technology allows investors to efficiently map frameworks and regulatory labels across jurisdictions so organizations can understand how the same product can be viewed in a variety of different perspectives.

Understanding the challenges and pitfalls of cross-border regulations is essential but unless we can solve that challenge, efficiently and at scale, then we will continue to see confusion and frustration. Technology can be one important way to combat limited regulatory alignment and ensure that investors remain safe from those who may exploit this environment; which would result in a poor outcome for investors, markets and the transition to a sustainable economy.