Key Takeaways

- In May 2024, ESMA finalized its long-awaited guidelines on the use of ESG or sustainability-related terms in fund names, commonly referred to as its fund “names rule”. The guidelines, originally consulted in November 2022, introduce requirements on funds that use ESG or sustainability-related terms in their names.

- New research by Clarity AI shows that, of a sample of roughly 3,200 funds, more than half contain breaches of the PaB exclusionary criteria, and would therefore need to divest assets or change their funds’ names to comply with ESMA’s guidelines around the use of ESG terms in fund names.

- Identifying breaches, particularly related to UNGC and OECD guidelines, is complex due to subjective criteria and limited data availability. Asset managers need reliable data tools, like Clarity AI’s screening solutions, to ensure compliance.

Three-month deadline to implement ESG guidelines confirmed for ESMA fund names rule

Time is running out for funds to comply with the ESMA fund names rule—ESMA’s guidelines around the use of ESG terms in fund names. Clarity AI research shows that more than half of the impacted funds are exposed to companies in breach of the Paris-aligned benchmark (PaB) criteria and will have to either divest from certain companies or industries, amend the name of their products, or otherwise risk falling short of the guidelines’ expectations.

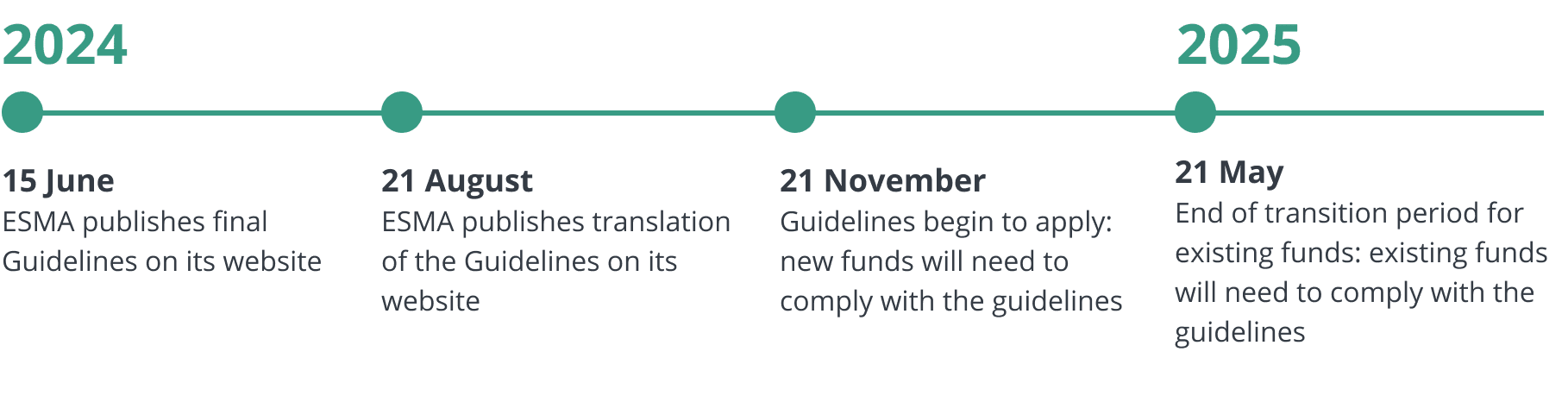

On 21 August 2024, ESMA published the translation for its long-awaited guidelines on the use of ESG and sustainability-related terms in funds’ names. The translation kick-starts the clock for asset managers to comply with the guidelines: new funds will have three months to comply with the guidelines and existing funds already authorized in the EU will have a further six months.

Previous Clarity AI research had shown that 44% of funds using environmental and impact-related terms in their name and therefore captured by ESMA’s naming rules may fall short of the guidelines due to exposure to companies active in tobacco, controversial weapons, or fossil fuels, and companies using inefficient energy generation techniques. New research by Clarity AI shows that – when including breaches of the United Nations Global Compact (UNGC) Principles and the Organisation for Economic Cooperation and Development (OECD) Guidelines for Multinational Enterprises (MNE) – that figure rises to 55%. In other words, of a sample of roughly 3,200 funds, more than half contain breaches of the PaB exclusionary criteria, and would therefore need to divest assets or change their funds’ names to comply with the guidelines.

Background to the guidelines

In May 2024, ESMA finalized its long-awaited guidelines on the use of ESG or sustainability-related terms in fund names, commonly referred to as its fund “names rule”. The guidelines, originally consulted in November 2022, introduce requirements on funds that use ESG or sustainability-related terms in their names.

The guidelines stipulate that any fund using a captured ESG or sustainability-related term in its name has to ensure that 80% of its assets are invested to meet either (i) the fund’s sustainability objective (in the case of Article 9 funds), or (ii) the fund’s environmental or social characteristics (in the case of Article 8 funds). Article 6 funds will need to consider upgrading to Article 8 or 9, or otherwise removing ESG-related terms from their names.

Funds must also apply exclusionary criteria to 100% of their assets depending on the term used. For funds using transition, social or governance terms in their names, asset managers must apply the climate transition benchmark (CTB) exclusionary criteria1. For those using broad sustainability, environmental or impact, they must ensure that their portfolio assets are not exposed to companies in breach of the PaB criteria2.

Figure 1: Paris-aligned Benchmark exclusions, contained in new ESMA funds’ names guidelines

Paris-aligned Benchmark exclusions, contained in new ESMA funds’ names guidelines

- (a) companies involved in any activities related to controversial weapons;

- (b) companies involved in the cultivation and production of tobacco;

- (c) companies that benchmark administrators find in violation of the United Nations Global Compact (UNGC) principles or the Organisation for Economic Cooperation and Development (OECD) Guidelines for Multinational Enterprises;

- (d) companies that derive 1% or more of their revenues from exploration, mining, extraction, distribution or refining of hard coal and lignite;

- (e) companies that derive 10% or more of their revenues from the exploration, extraction, distribution or refining of oil fuels;

- (f) companies that derive 50% or more of their revenues from the exploration, extraction, manufacturing or distribution of gaseous fuels;

- (g) companies that derive 50% or more of their revenues from electricity generation with a GHG intensity of more than 100 g CO2 e/kWh.

There are also specific requirements for funds using sustainability, transition or impact-related terms.

Terms

Exclusions*

Aditional Requirements

*All captured funds must demonstrate that 80% of its assets are invested to meet either (i) the fund’s sustainability objective (in the case of Article 9 funds), or (ii) the fund’s environmental or social characteristics (in the case of Article 8 funds).

Reaction to the guidelines

These guidelines, therefore, seek to ensure funds “do what they say on the tin” by implementing some minimum requirements around funds that promote ESG characteristics by using related terms in their names. This in turn supports transparency towards retail investors by aligning fund names with the companies they invest in. Implementing the guidelines in practice, however, may prove to be more challenging than expected.

Asset managers will require granular data on investee companies to ensure they do not invest in companies breaching the exclusionary criteria mentioned above, and therefore fall short of supervisory expectations. Further complexity is also likely to arise in the case of funds investing in “green bonds” whose use of proceeds is intended for sustainability purposes, but whose issuer may still be at the beginning of their transition journey and exposed to legacy business lines that breach PaB exclusionary criteria.

Despite pushback from the market, ESMA has confirmed that making such investments does not circumvent the requirement for the issuing company to adhere to the Paris-aligned benchmark exclusionary criteria. This could lead to further divestments or pressure to remove ESG terms from certain funds’ names.

Clarity AI research

In our previous article, we examined funds with environmental and impact-related terms in their name and how they adhered to PaB exclusionary criteria (a), (b), (d), (e), (f), and (g). These exclusions relate to investee companies’ exposures to fossil fuel, tobacco, controversial weapons, and companies whose revenue comes from inefficient energy generation techniques3. We found that nearly half – 44% – of funds whose names would be captured by the rule are exposed to at least one company in breach of those criteria. In this second article, we examine criteria (c) – companies in violation of the UNGC Principles or the OECD Guidelines.

We examined UNGC and OECD MNE violations in isolation to highlight the challenge financial market participants may face in trying to determine what constitutes a violation – commonly referred to as a “breach”. Breaches of these global norms are inherently more subjective than the revenue-based exclusions examined in part 1 and so far the regulatory guidance for identifying violations has been thin on the ground.

What constitutes a violation of UNGC and OECD MNE?

In the absence of concrete advice from policymakers and regulators, the Platform on Sustainable Finance – an influential group advising the European Commission on the development of its sustainable finance regulatory framework – has partly filled the regulatory void. To identify breaches, the Platform suggests identifying instances where a company has been “held liable” or found “in breach” of labor law or human rights in a court of law4. This reliance on court judgments has merits as it avoids companies being found guilty in the “court of public opinion” and also reduces the likelihood that a company is found in breach of something that it later proves its innocence against.

Finding information from court cases is not, however, straightforward. Companies are not always forthcoming about reporting such violations. Through the roll-out of the EU’s Corporate Sustainability Reporting Directive (CSRD) and the increase of companies reporting under the European Sustainability Reporting Standards (ESRS)5, we may see improved data on companies related to UNGC and OECD MNE breaches. Nevertheless, as of today, many are not required to report such violations and may lack incentives to do so due to the potential negative publicity.

Other factors also add complexity to the process of identifying a UNGC or OECD MNE breach – has the company settled with any claimants or victims? Has the company launched an appeal? How long ago did the breach occur and how long should it be valid for? How severe is the breach? Relying on external sources – either research or through a third-party data provider – is therefore important.

Clarity AI approach to UNGC and OECD breaches

To overcome these challenges, Clarity AI leverages advanced Natural Language Processing (NLP) to detect ESG-related controversies associated with companies that could potentially violate the UNGC principles or the OECD MNE guidelines. NLP models are applied to over 30,000 trusted news sources, reviewing as many as 100,000 articles per day to detect such controversies.

Breaches are detected and flagged based on stringent criteria. For an incident to be considered a breach, it must be supported by concrete legal evidence of the company’s culpability. This includes situations where the company has been found guilty or liable by a court or a regulatory authority, or where there has been a public admission of guilt by the company itself. The process further considers the severity of the incident and any remediation activities initiated or implemented.

Data freshness is very important in detecting breaches: since the publication of our first article in May, we have detected five new breaches, three of which relate to automotive companies that cumulatively appear in more than 500 funds with impacted terms.

Below are some illustrative examples of breaches identified by the NLP model.

This approach ensures that all flagged breaches are substantiated by definitive legal evidence, focusing on the severity of each incident to identify violations. It aligns with the Platform on Sustainable Finance’s recommendations, confirming the robustness and relevance of the approach in upholding rigorous standards for corporate responsibility.

Clarity Al approach to UNGC and OECD breaches

NPL Model detects potential violations

The process further considers the severity of the incident and any remediation activities initiated or implemented

![]()

Severe incidents sent for further evaluation

This approach ensures that all flagged breaches are substantiated by definitive legal evidence

![]()

Specialized analysts review and apply methodology criteria

This method provides clear, reliable insights into corporate compliance with ESG standards

![]()

Status of UNGC / OECD violation is confirmed

It aligns with the Platform on Sustainable Finance’s recommendations, confirming the robustness and relevance of the approach

Implications for ESMA fund name guidelines

So how does the inclusion of these breaches impact our results from our first analysis on ESMA’s guidelines on fund names?

Adding the data on UNGC and OECD MNE breaches to our first analysis expands the number of companies that violate the PaB exclusions. As a result, we find that – from our sample of 3,200 funds with environmental and impact-related terms in their names – 55% could fall short of ESMA’s new guidelines. This means more than half of the funds in our sample would need to divest assets, change their name or risk falling short of supervisory expectations.

Overall, we found that 36% of funds across the universe of impacted products contained OECD or UNGC breaches. These breaches come from a variety of sources, primarily driven by concerns around quality and safety, as well as anti-competitive practices. The full breakdown is as follows:

Figure 2: Breakdown of breach type by funds affected

These beaches are driven by 22 companies that are invested in by many funds. Those companies are based mostly in the European Union, United States and Asia, with some presence in Latin America and the United Kingdom. They cover a range of sectors, with most breaches coming from consumer, industrial materials, and communication sectors.

The implication of the new guidelines, therefore, is that funds will need to screen more carefully even large companies that appear in their financial products. It also suggests that by engaging and improving practices in a small number of companies, asset managers can increase their investable universe.

Figure 3: Location of companies found in breach of UNGC and OECD MNE

Figure 4: Sector of companies found in breach of UNGC and OECD MNE

Conclusion

On 21 August 2024, ESMA translated its guidelines on the use of ESG terms in fund names into official EU languages. In doing so, it kickstarted a three-month clock for funds to adhere to the guidelines.

Clarity AI research suggests that more than half of funds impacted by the guidelines may need to change their name, divest assets or risk falling short of supervisory expectations. The path to compliance, however, is not simple.

Firstly, identifying beaches of exclusionary criteria relies on granular data and continuous monitoring of investee companies. In the case of UNGC and OECD MNE breaches, this can be particularly challenging given the lack of regulatory advice and subjectivity in determining what is a breach, and the speed by which the data needs to be refreshed. Therefore, it is important to rely on external sources—whether through their own research or a third-party data provider—to ensure accurate and comprehensive information.

Secondly, as an asset manager, understanding which companies you are invested in is extremely important. Companies may be exposed to different revenue lines or in breach of the UNGC or OECD MNE. This is doubly important given ESMA’s clarification that the guidelines hold equally for equity exposures, and also where funds are exposed to companies via green bonds. This means that, even where the use of proceeds is intended for sustainability purposes, asset managers will need to assess the issuer to ensure that they are not in breach of UNGC or OECD MNE or otherwise engaged in activities prohibited by the PaB exclusionary criteria.

Overall, ESMA’s guidelines are likely to have a big impact on the market. Asset managers do not have long to ensure that their products adhere to the guidelines.

Clarity AI leverages cutting-edge technology to provide sustainability-related insights to financial market participants. Our PaB exclusion tool allows you to quickly scan your portfolio for exposure to companies with PaB exclusion breaches, including those related to UNGC and OECD MNE. We offer comprehensive PaB screening tools that include all necessary metrics, aggregated results, and detailed evidence from company reports, including PDF links and explanatory notes from our sustainability experts.

Contact us to learn more about our solutions and how we can assist you in addressing the new ESMA guidelines.

- The CTB criteria are a subset of the PaB criteria, covering (a), (b) and (c) in Figure 1

- See Commission Delegated Regulation (EU) 2020/1818 Article 12 for list of exclusions

- See Figure 1 for full list of exclusionary criteria

- See, for example, Platform on Sustainable Finance Final Report on Minimum Safeguards (October 2022)

- See Delegated Regulation (EU) 2023/2772