Starting January 2024, companies are required to report on eligibility for all 6 environmental objectives of the EU Taxonomy

The European Union has been at the forefront of global environmental initiatives, from its ambitious climate goals to its pioneering regulatory initiatives. One of its key initiatives is the EU Taxonomy, a framework for categorizing environmentally-sustainable economic activities. This tool aims to boost sustainable investments and to accelerate the shift to a low-carbon, resource-smart economy. Its initial emphasis centered on two climate goals: climate change mitigation and adaptation.

However, as of January 1st 2024, companies will be requested to start reporting eligibility for the remaining four environmental objectives of the EU Taxonomy: “Sustainable use and protection of water and marine resources,” “Transition to a circular economy,” “Pollution prevention,” and “Protection and restoration of biodiversity and ecosystems.”

A Final Version with Less Activities

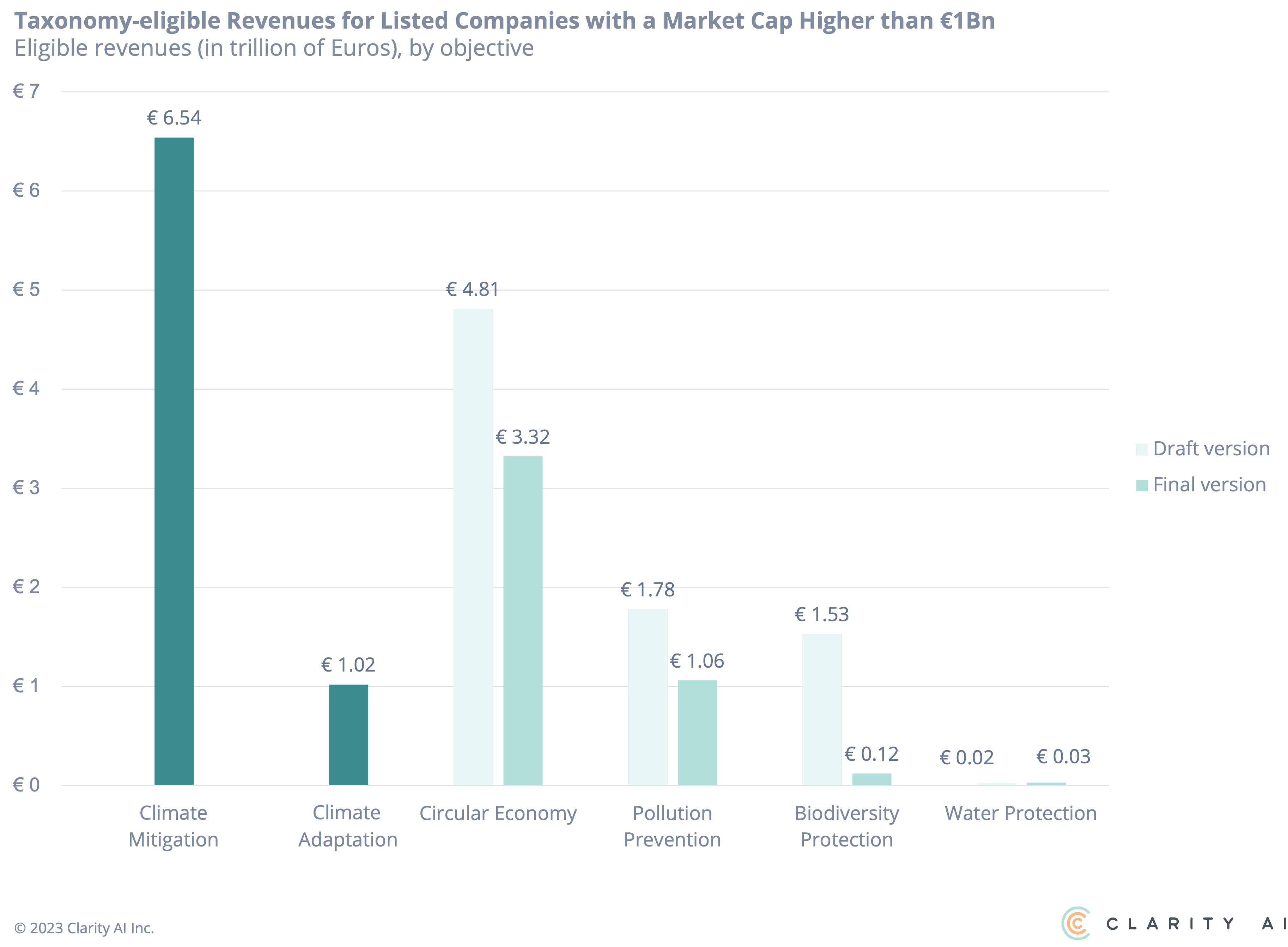

The activities finally included in the four new environmental objectives have undergone notable changes from the draft versions proposed in March 2022. These amendments highlight the difficulty of finding compromise among Member States with different priorities. As a result, the final version of the objectives decreased the portion of revenue eligible by 45%, compared to the draft version.

The “Transition to a circular economy” objective, for instance, no longer includes activities such as furniture manufacturing, or clothing and footwear production , while “Pollution prevention and control” dropped activities like chemical manufacturing.

The scope of “Protection and restoration of biodiversity and ecosystems” objective was also reduced. In the draft version, it included activities related to the agricultural sector such as crop and animal production, which were discarded in the final version of the Delegated Act.

A Balancing Act: Climate vs. Environment

Despite the addition of four new objectives, EU Taxonomy’s revenue eligibility still favors the two initial climate change objectives. This is evident, as an example, considering Taxonomy-eligible revenues for highly relevant listed companies (market cap higher than €1Bn).

The “Transition to a circular economy” and “Pollution prevention and control” objectives show good results. However, “Climate change mitigation” remains the largest opportunity, in terms of eligible turnover for the Taxonomy.

The official implementation of the four non-climate objectives represents an indicative step towards a more comprehensive and all-encompassing approach to sustainability, in which each dimension is recognized and valued.

While data indicates that “Climate change mitigation” remains the predominant objective, this emphasis aligns with the EU’s primary commitment to the Paris Agreement upon launching the EU Taxonomy project. Furthermore, it’s important to recognize that a balanced approach to environmental sustainability doesn’t necessarily translate into equal eligible revenues for all objectives.

The Road Ahead

The EU Taxonomy, as a whole, remains a work in progress. Essential areas such as crop cultivation and livestock farming have not been fully integrated. Moreover, the mining sector, pivotal for renewable technologies, is yet to be included. This point gains further importance with the EU’s recent publication of the Critical Raw Materials Act.

However, the evolving nature of the tool is a testament to the EU’s dedication to keep improving a robust framework that genuinely drives sustainability. Investors need to stay updated and, potentially, be ready to recalibrate their portfolios to match the Taxonomy’s expanding goals.

The European Union remains a pioneer, setting the standard for other regions to follow. In merging climate change objectives with broader environmental goals, it showcases the nuanced, interconnected nature of the planet’s challenges.