The Financial Conduct Authority (FCA) established the Sustainability Disclosure Requirements (SDR) to enhance transparency in sustainability-related disclosures for financial products. For UK asset managers, it was a regulatory step-change with the SDR forming an important part of their sustainability reporting requirements since its progressive introduction from May 31st, 2024 onwards.

As part of the SDR’s rollout, its sustainability fund labels were launched on July 31st, 2024. The next major deadline was December 2nd, 2024 when the naming and marketing rules came into force. This guide outlines the key steps for UK asset managers to comply with those requirements when labeling their sustainability funds or using terms captured by the naming and marketing rules.

Departing from the EU’s Disclosure Regime: FCA Fund Labels in the UK

On November 28th, 2023, the FCA published its long awaited SDR and investment labels policy statement (PS23/16). The policy statement introduced regulations which impact all regulated financial entities in the UK and address key weaknesses that many see in the EU’s Sustainable Finance Disclosure Regulation (SFDR).

A significant change is the introduction of clear, explicit labels for sustainable funds. This differs from the SFDR’s disclosure-focused approach and aims to help investors more easily understand and navigate sustainable investments. The resulting SDR labels set a high bar for all sustainability claims and are designed to combat greenwashing.

Given the SDR’s marked differences versus the SFDR, it’s not possible for UK asset managers to rely upon their current SFDR disclosure classification (e.g. Article 8 or Article 9) to meet the SDR’s labeling criteria. A targeted SDR labeling approach is needed.

Currently, the SDR only applies to UK funds at this stage. Overseas funds are not affected yet, although the UK Government indicated that it will communicate on whether the SDR labeling regime should be extended to cover offshore funds in the future.

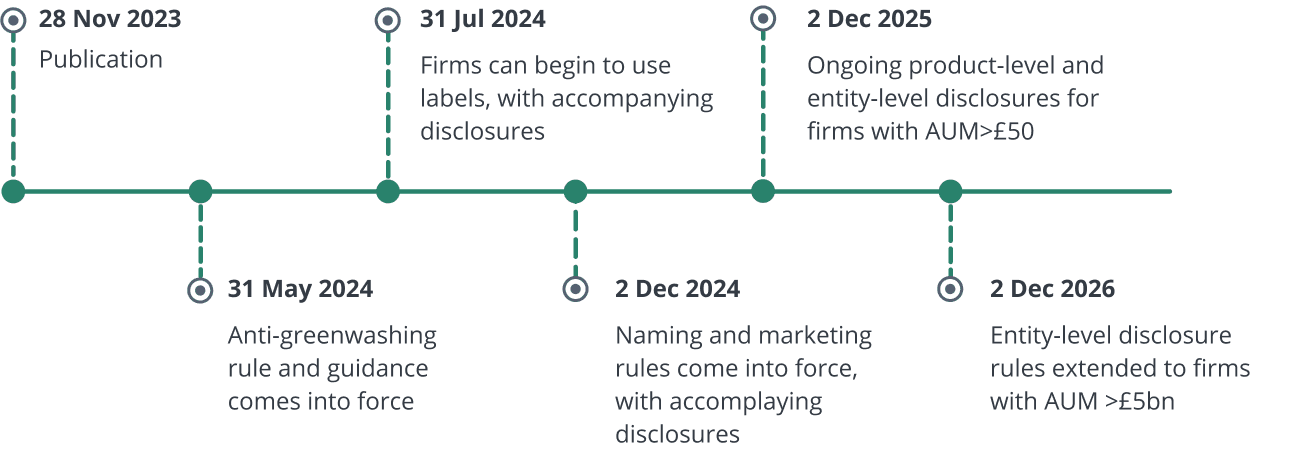

UK SDR Fund Label Implementation Timeline

The SDR established four sustainability labels, which became available for use starting July 31, 2024. Funds without these labels that incorporated sustainability-related terms in their names or marketing materials were required to comply with the naming and marketing guidelines by December 2, 2024. However, the FCA announced temporary flexibility in September, giving certain asset managers an extension until April 2025 to meet these requirements.1

This requires funds to do one of the following:

(i) Begin using a sustainability label, or

(ii) Provide extra disclosures outlining why they do not use a label and justifying their use of sustainability language, or

(iii) Removing sustainability terminology from their name and marketing materials.

Figure 1. UK SDR Implementation Timeline

General Qualifying Criteria for UK SDR Labels

There are four general qualifying criteria for all investment products aiming to use SDR labels:

-

Sustainability objective

Products using an SDR label must disclose their objective regarding environment or social outcomes. UK asset managers must also disclose if pursuing those positive sustainability outcomes may result in any material negative outcomes.

-

Investment policy and strategy

At least 70% of a product’s assets must be invested in alignment with its sustainability objectives, referencing a “robust, evidence-based standard that is an absolute measure of environmental and/or social sustainability”. UK asset managers must also disclose any other assets held in the fund for other reasons (e.g., cash, derivatives), including why they are held.

-

Key performance indicators (KPIs)

Asset managers must identify relevant KPIs to measure the progress of their sustainability objectives, and regularly report on these to investors.

-

Stewardship and escalation

Asset managers must disclose the stewardship strategy needed to achieve their sustainability objectives. Firms must also set an escalation plan for when assets do not demonstrate sufficient progress towards their sustainability objective or KPIs.

The 7 Steps for Asset Managers Using Sustainability Fund Labels to Comply With the UK SDR

Complying with the SDR’s sustainability fund labeling and naming & marketing rules requires a systematic approach from UK asset managers which is best integrated into their broader sustainability strategies. Let’s examine the seven steps required to comply with the SDR’s requirements when reporting fund labels.

Step One: Select the Right SDR Fund Label

As a starting point, UK asset managers must familiarize themselves with the SDR’s four distinct fund label categories (Exhibit 1). The labels are not hierarchical and instead represent differing sustainability objectives and investment approaches. Across the four labels, 70% of the gross value of the product’s assets should be invested in line with the sustainability objective, allowing 30% to be used for other purposes such as liquidity and risk management.2 All labeled funds must make consumer facing, pre-contractual and ongoing product disclosures.

Exhibit 1. UK SDR Fund Category Labels

[code_snippet id=84]

Step Two: Assess Existing Funds Against the Labels and Naming and Marketing Rule

The next step for UK asset managers is to evaluate each fund in their portfolio to determine its alignment with the SDR label categories and the naming and marketing rule.

The following should be considered:

- The asset manager’s investment and sustainability objectives.

- The fund’s investment and sustainability objectives.

- The nature of the fund’s underlying assets.

- The asset manager’s sustainability expertise and experience.

- The Environmental, Social, and Governance (ESG) criteria integrated into the investment process.

Step Three: Develop Clear Disclosures

Next, UK asset managers should prepare clear and concise disclosures either for each SDR fund label they use, or for those captured by the naming and marketing rules, including:

- The sustainability objectives of the fund.

- How the fund meets the criteria for its chosen label.

- The relevant KPIs, metrics or benchmarks used to assess the product’s sustainability performance.

Step Four: Implement Robust Governance

UK asset managers should also establish robust governance structures to oversee the SDR fund label compliance process, including:

- Designating a responsible team or individual for SDR compliance.

- Regularly review and update SDR fund labels and disclosures as necessary.

Step Five: Engage with Stakeholders

UK asset managers should communicate with their stakeholders, including investors and regulators, about their fund sustainability labels and practices. Transparency is key to building trust and credibility about the SDR labels.

Step Six: Monitor and Report

UK asset managers should continuously monitor the performance of their funds against their sustainability objectives. These metrics and KPIs should be reported on as part of ongoing compliance with the SDR’s requirements. Additionally, firms must specify a measurable sustainability objective and determine the KPIs they will use to measure performance toward that objective. The FCA does not provide specific prescriptions for which KPIs should be used, as firms will need to determine which metrics are most appropriate for their products.

Step Seven: Stay Informed

Finally, UK asset managers should keep abreast of any updates or changes to the FCA’s SDR framework by regularly reviewing guidance documents and participating in industry discussions to ensure ongoing compliance.

How Clarity AI Can Support UK Asset Managers Aligning with the SDR

Clarity AI is a market leader in developing a bespoke solution for fund labeling under the SDR. As a result, Clarity AI can help support UK asset managers to align with the SDR in a number of ways:

- By enabling asset managers to evaluate their SDR eligibility, and thus label their products in line with the SDR regulations.

- By enabling asset managers to define, describe, and communicate their sustainability objectives – and use of any SDR label – by mapping their fund’s objective and strategy to specific data points and KPIs that can be used to monitor and evidence its performance.

- By supporting adherence to the naming and marketing rule by providing metrics and KPIs to justify the use of sustainability terms in unlabelled funds.

- By providing access to a vast dataset covering 70,000+ companies, 430,000+ funds, and 400 national and local governments, depending on the selected KPI.

- By offering a wide range of sustainability metrics, including Climate Temperature Alignment, SFDR PAIs, EU Taxonomy Alignment, and SDGs Revenue Alignment.

- By providing flexible, transparent, and customized data through an easy to use user interface to enable the development of different fund strategies and objectives.

- By monitoring sustainable regulatory developments that could impact asset managers, and wherever relevant engaging in the development of such regulations.

UK SDR Fund Labels Are a Major Development

The UK SDR is a major development for sustainable finance regulation globally. Importantly, the SDR’s labeling regime marks a clear departure from the EU’s SFDR and is an approach that could be copied by regulatory bodies elsewhere in the coming years.

UK asset managers can successfully navigate the SDR’s labeling regulations with a systematic approach which is best integrated into their sustainability strategies. The steps mentioned in this guide are likely to help with that process.

References

- Financial Conduct Authority. “FCA Sets Out Temporary Measures for Firms on ‘Naming and Marketing’ Sustainability Rules.” FCA, September 9, 2024. https://www.fca.org.uk/news/statements/fca-sets-out-temporary-measures-firms-naming-and-marketing-sustainability-rules

- Financial Conduct Authority. Sustainability Disclosure Requirements (SDR) and Investment Labels. Policy Statement PS23/16, November 2023. https://www.fca.org.uk/publication/policy/ps23-16.pdf.

- Ibid.

- Ibid.

Author Information