Using natural language processing for improved EU Taxonomy solutions

As a common classification system for sustainable economic activities, the EU taxonomy is a pioneer in the field and will be instrumental in achieving the emissions reduction and mitigation goals of the European Union’s Green Deal.

It defines which economic activities can be considered environmentally sustainable related to six environmental objectives: (1) climate change mitigation, (2) climate change adaptation, (3) sustainable use and protection of water and marine resources, (4) transition to a circular economy, (5) pollution prevention and control, and (6) protection and restoration of biodiversity and ecosystems. A forthcoming social taxonomy will define objectives beyond the environment.

This taxonomy is used for, among other things, labeling financial products and corporate bonds marketed as environmentally sustainable. Under the Sustainable Finance Disclosure Regulation (or SFDR), investors need to report their alignment to the EU taxonomy as part of the sustainability profile of their funds, which are classified into one of three categories:

- ARTICLE 6: non-sustainable funds

- ARTICLE 8: funds that promote sustainable characteristics but not as an overarching objective

- ARTICLE 9: funds that have been specifically created to address sustainability goals

Challenges for Compliance

Complying with the EU Taxonomy is not easy. Specifically, investors face two major challenges:

- Conflict between data availability and need. In 2022, the EU taxonomy requires investors to report product alignment to the climate adaptation and mitigation objectives—and the other four environmental objectives will be required by 2023. However, companies will not report alignment until 2023. This data availability mismatch will persist for the foreseeable future, as a limited number of companies will be covered by the European Commission’s Corporate Sustainability Reporting Directive (CSRD) and will therefore report in line with the EU taxonomy.

- Methodology development is an ongoing process. This is true of the released climate objectives, in which there are differences in interpretations across companies and countries (such as the inclusion of natural gas and nuclear as green activities). Investors need to be ready to adapt and respond to a complex landscape of evolving regulations.

How to source the data?

Investors’ success at bridging the data gap will vary. The implementation of the CSRD will help, eventually compelling close to 50,000 companies to report sustainability performance on a comprehensive set of metrics. But the CSRD will not be fully implemented by 2025, and non-EU jurisdictions are likely to lag even further behind.

In a world that moves as fast as ours does, using the power of AI—specifically natural language processing—helps to ensure, at scale, the detection of incidents and the severity of those incidents. Therefore, in the absence of technology, the reliability of EU taxonomy assessments could suffer.

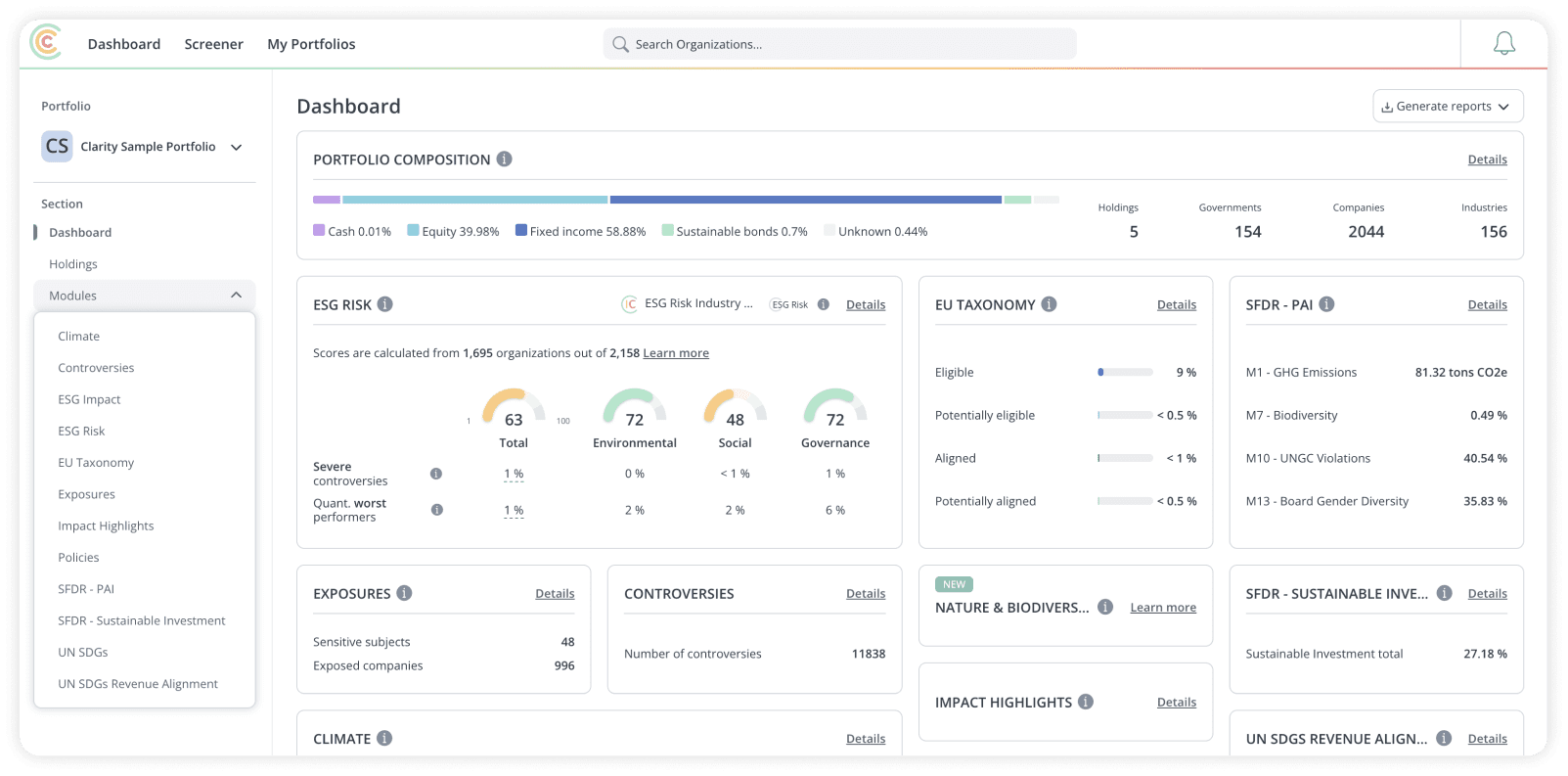

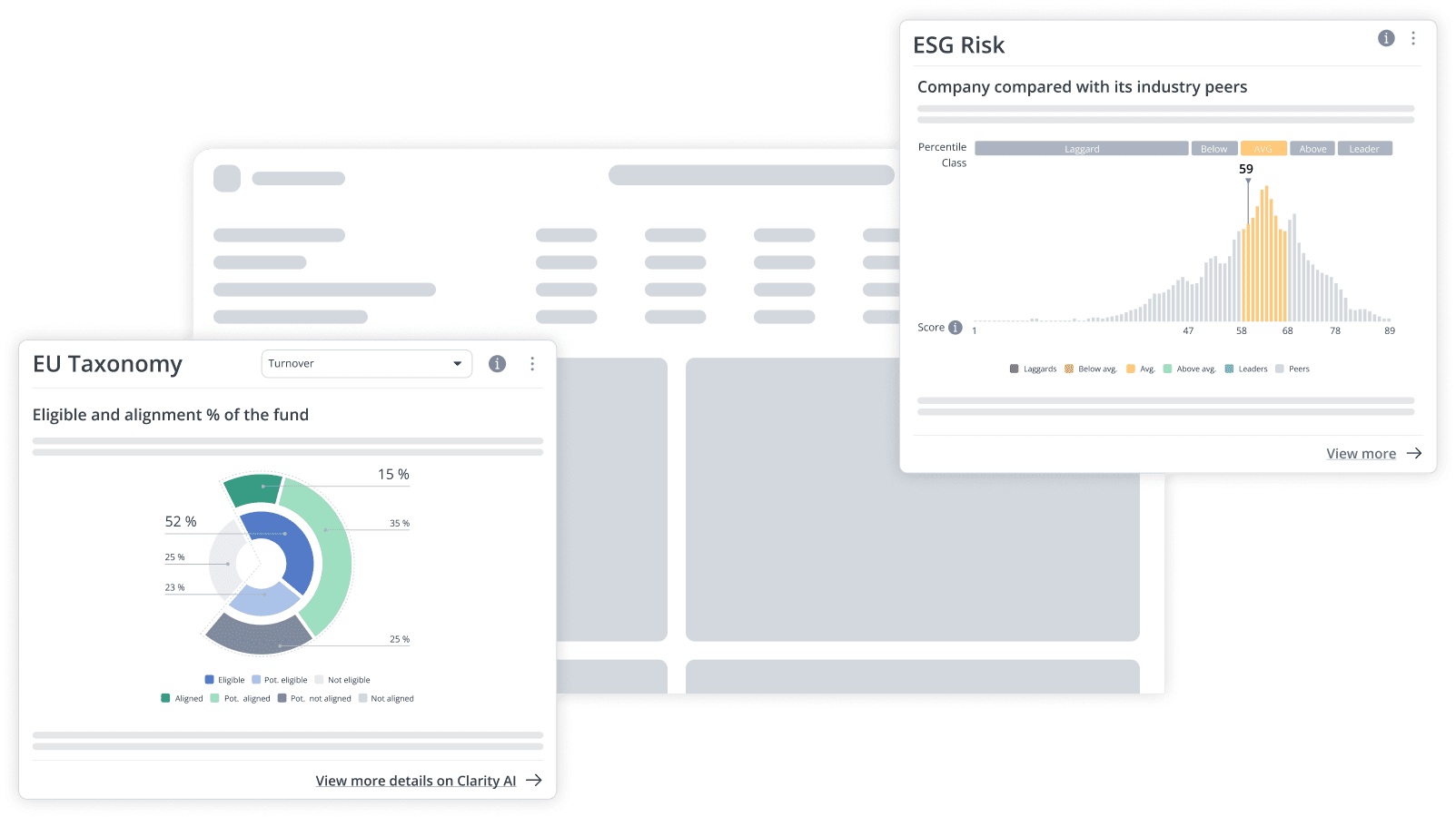

To analyze the alignment of each portfolio company, Clarity AI follows a five-step approach. This analysis provides two key metrics that investors will need to report:

- percentage of eligible green revenue, as defined by revenues eligible for the activities outlined in the EU taxonomy

- percentage of aligned green revenue, which builds upon eligible activities and embeds an assessment of the technical screening criteria, DNSH and SS requirements.

But what does this look like in action? The case study below provides one specific example of the merits of a scalable approach for EU taxonomy reporting.