EU Regulation: The latest extension to the MiFID II directive explained

An extension to MiFID II is one of the key components of the comprehensive European Commission’s sustainable finance regulatory agenda, alongside SFDR, EU Taxonomy and CSRD.

Among a host of new MiFID II requirements is one major change – distributors and financial advisers must incorporate sustainability preferences in the overall client suitability assessment.

This new requirement will have ramifications for market participants, such as:

- Though the burden is on the advisers, it also applies to asset managers since they will be required to disclose the information that advisers need

- An even larger increase in scrutiny around greenwashing as advisers will also set a bar in terms of the sustainability products selected

While these regulations have laid the foundations for the development at scale of sustainable investing, MiFID II can be seen as the crown of the edifice. By placing end investors’ sustainability preferences at the core of the investment process, this regulation will trigger a radical transformation of the investment industry – a transformation with ramifications that even the largest players in the market might not yet fully understand. We see three key reasons why MiFID II opens a new paradigm for sustainable investment:

- “Of the People” – Efficient frontiers and asset allocation will need to be revisited to account for the “impact” third dimension

- “By the People” – End investors will play a key role in setting the sustainability performance targets throughout the investment process

- “For the People” – There will eventually be no room for fund with no clear impact targets

Of the People

First, MiFID II is nothing less than a copernican revolution. For many years, the development of sustainable investing has been hampered by the debate about whether or not it is consistent with fiduciary duty. The PRI and UNEP FI have published over the years a series of seminal reports to address this issue and to highlight ways to manage it. With successful results around accounting for ESG related financial materiality, PRI’s extended its effort recently to impact investing. MiFID II brings to Europe a singular and definitive answer to this debate by giving life to sustainable investment of the people. Under MiFID II, Investment firms will be held accountable not only for delivering the financial performance corresponding to the risk profile of their final beneficiaries, but also to the expected level of societal impact matching those financial beneficiaries’ sustainability preferences.

As a consequence, investors will have to navigate uncharted territory and upgrade the tools they use to navigate successfully. The long-lived modern portfolio theory of the risk-and-return efficient frontier will need to be expanded to add a third dimension: “societal impact.” Investment products’ performance will be assessed on total return (i.e., financial return and social return on investment [SROI]). To efficiently manage the trade-offs along these three dimensions, product design will require the development of new tools.

Strategic Asset Allocation might also need to be revisited to optimize the desired SROI, as the ability to generate and evidence impact varies significantly among asset classes.

- Real assets such as infrastructure and real estate can generate direct measurable impact.

- Green and sustainable bond issuances benefit from intentionality and measurability frameworks likely to deliver impact.

- Private equity investments can both entail the promise for higher innovation potential and for greater efficiency of engagement with the founders to ensure sustainability performance than for public companies.

Relying on relevant impact data sets will also prove to be a core requirement. Characterizing impact on a specific sustainability matter requires evidence metrics that can be significantly different from financial materiality assessment. Investment firms will need to ensure that the data they rely upon is data that are fit for MiFID II purposes. Three characteristics will need to be considered:

- The level of granularity and specialization

- The monetization of the social value created

- The identification of change leaders

By the People

Second, once the pandora box of individuals’ sustainability preferences is opened, expectations will continue to increase when taking into account financial beneficiaries’ wants.

Sustainability preferences are already multi-facetted, and they are evolving quickly. This can lead to as many preferences as investors. They also often rely on partial information and biased perceptions. In a study conducted in France and Germany, 2° Investing Initiative found that sustainability preferences vary depending on age, gender, revenues, voting habits, geography and also on the way questions to be answered by final investors were framed. Since these preferences reflect individual core values, the associated expectation for alignment will prove to be particularly high, and investments will need to track closely that alignment over time.

To deal with this, the required level of interactivity with final investors will significantly increase. As investors are given a say in the type of impact to be delivered, thus “voting with their savings,” they will expect investment solutions to reflect more direct democracy than indirect democracy. This means that they will not only require the reporting of the actual impact performance in clear terms, but also they will expect to influence portfolio composition on a regular basis, including by contributing to engagement and voting or by reacting to news feeds and controversies. This will be sustainable investment by the people.

For the People

Last, MiFID II is likely to play out as the catalyst for an eventual switch to impact-only sustainable investment solutions. Double materiality lies at the core of the regulation. Product design should combine three dimensions:

- Sustainability risk integration (the alpha generation narrative)

- Exclusions (for value alignment through integration of Principle Adverse Impact indicators)

- Impact integration (EU Taxonomy and SFDR Article 9 targets).

However, product performance comparisons will likely focus on impact rather than sustainability risk integration, which will establish new rankings within sustainable investment for the people.

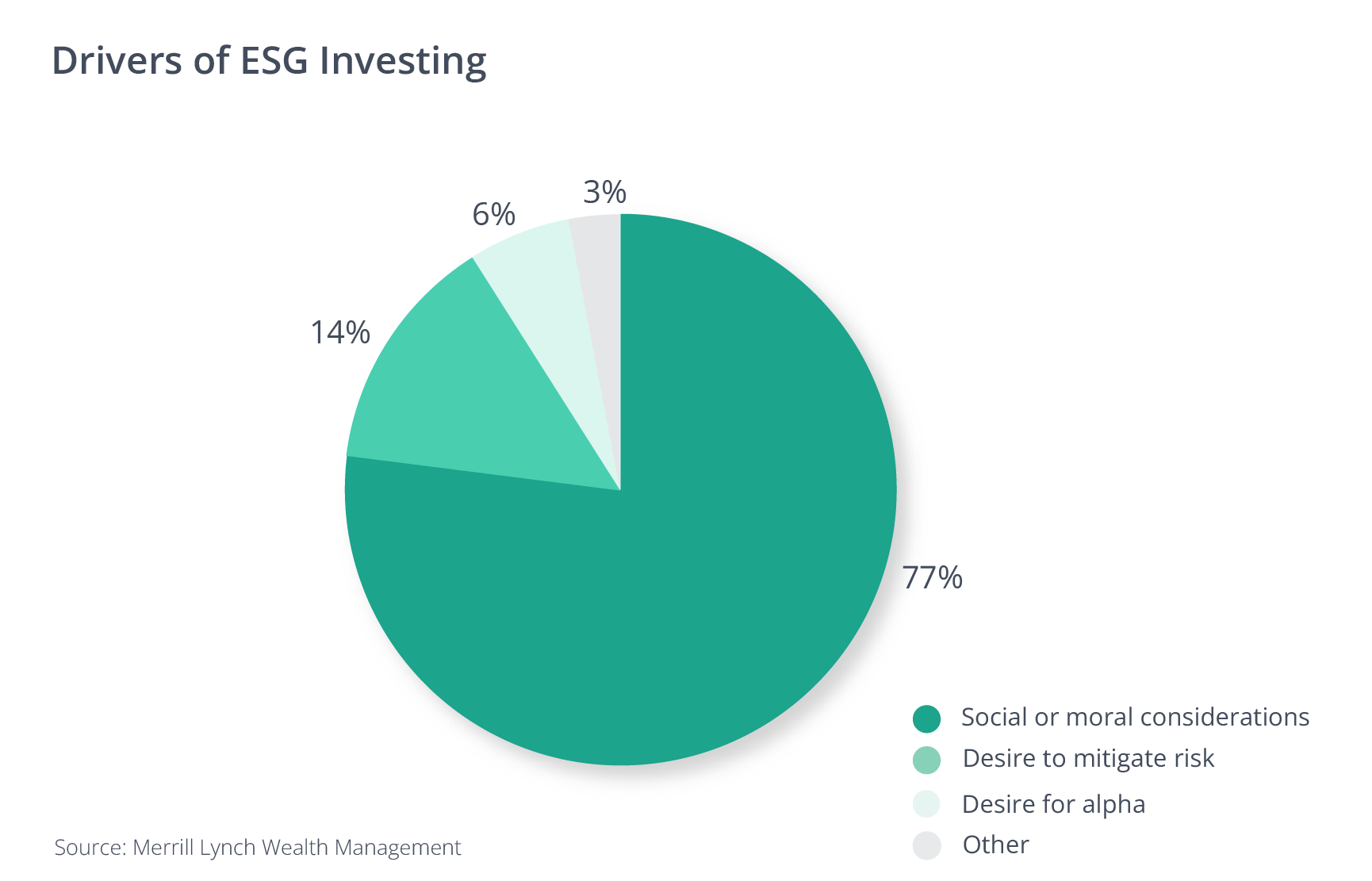

This development will leave little or no room for solutions without any impact credentials. Wealth managers have been leading the front to consider social and moral considerations, whereas asset managers have historically focused on increased returns to support ESG integration. This distinction is likely to rapidly vanish as evidence for impact will become the new normal.

Investment firms will need to learn how to overcome the tragedy of the horizons and to dynamically manage the frontier between sustainability risk and impact as regulation evolves. Firms will also face the necessity to align investment horizons and expected impact returns, as, depending on duration, the outcome potential might vary significantly.

Closing the Circle

Matching expectations of the impact promise implied by MiFID II is a one-of-its-kind challenge, with high risks of mis-interpretation, mis-selling and eventually, failure to deliver. It therefore requires Financial Market Participants and sustainability data and ratings providers to adjust their offerings.

MiFID II opens a new era of democratization of sustainable investment based on increased integrity, customization, reactivity and interactivity. Soon, investment solutions that yesterday were only accessible to highly sophisticated institutional investors will become available to the broader public.

At Clarity AI, we view technology as a key enabler of this much-welcome transformation. Thanks to our AI machine learning estimation models and extended NLP approach we have been able to develop unique specific metrics and coverage for SFDR and EU Taxonomy. Our platform also offers unprecedented functionalities to compare funds impact performance through multiple dimensions. Tech will empower the dynamic connection between investors’ sustainability preferences and actionable investment solutions, and it will facilitate the delivery of cost-efficient solutions at scale.

1. Fiduciary duty in the 21st century

2. A legal framework for impact

3. Climate VAR vs. Climate footprint when it comes to climate change integration for instance

4. The ability to evidence impact is a direct function of granularity. It also requires very specific approaches relying on in-depth sector expertise as demonstrated by hyper-specialized data providers focusing on biodiversity, gender, asset-level data, supply chain, employee satisfaction, product labels…

5. Impact can be achieved across many different dimensions of sustainability matters that are difficult to compare or aggregate. At portfolio level, optimization of impact on one specific dimension might be detrimental to the performance of another one. Methodologies that monetize impact are a key enabler of this necessary comparability to assess different impact trade-off options (HBS IWAI and Clarity AI SDG impact for instance).

6. The characterization of sustainability preferences might come short of reflecting preferences for investors eager to reach impact by driving change through exposure to companies which are underperformers but have taken measures to improve (policies, commitments, new sustainability risk management procedures) and/or can influence a whole sector. The World Benchmarking Alliance’s approach to identifying among keystone companies those leading positive systemic change in their sector might be an interesting solution to that regard.

7. The report also analyzed findings from previous similar studies conducted by Morgan Stanley, French AMF, UK DIFID, EU HLEG, Natixis, Schroders, and the University of Maastricht

8. Impact comparison of SFDR Article 9 funds is already happening