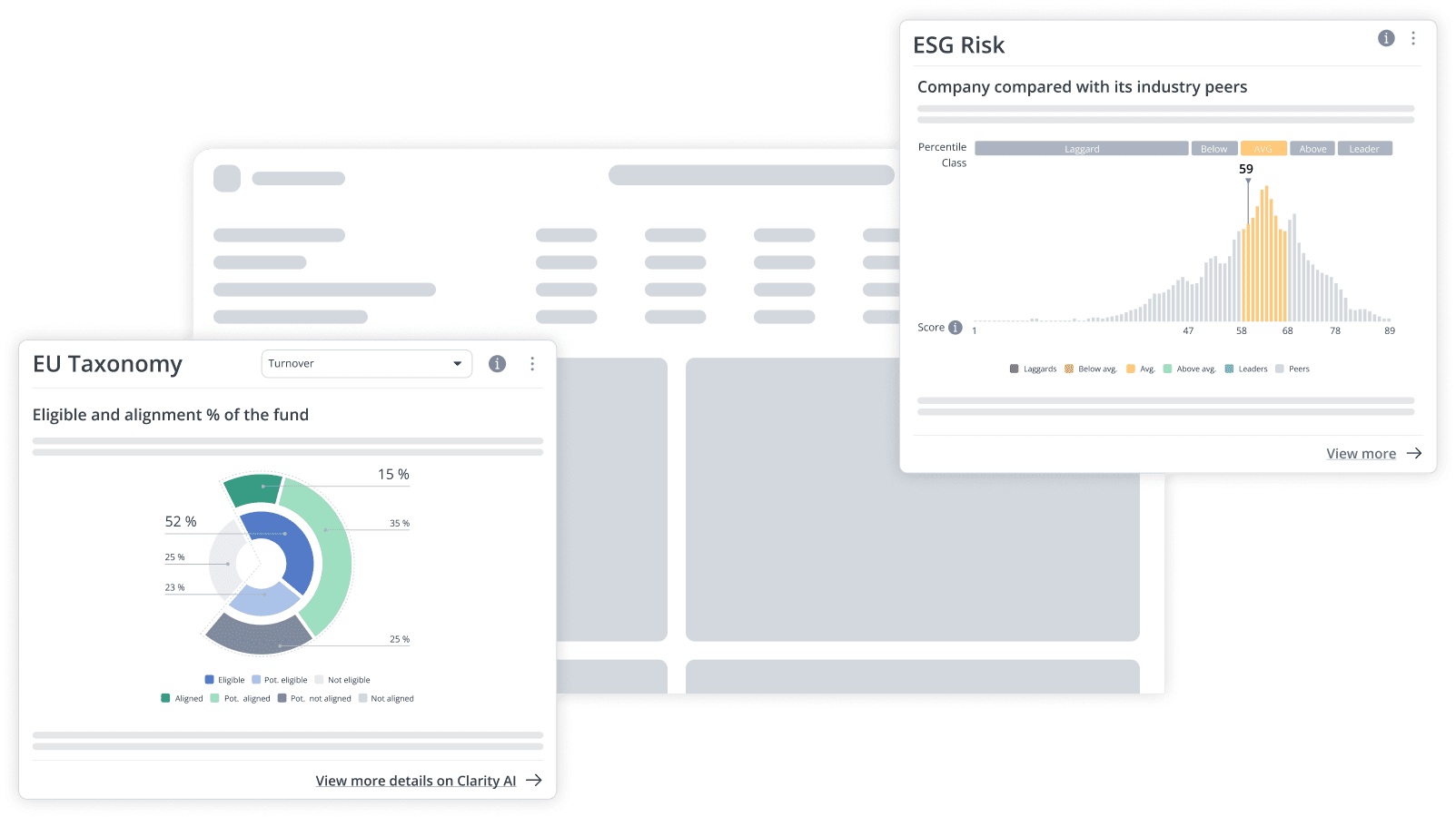

EU Taxonomy requires financial market participants to identify and exclude non-NFRD companies in their reporting

The “Non-Financial Reporting Directive (NFRD)” was created to bring more transparency into the social and environmental performance of large companies. The Directive sets out specific criteria on which type of companies should disclose non-financial information and the guidelines they should follow.

Specifically, companies that fall under any of these two categories are affected by the NFRD:

- Large listed companies, banks or insurance companies, that have;

- balance sheet total that exceeds €20 million or

- turnover that exceeds €40 million

- An average number of employees exceeding 500 during the fiscal year

It is important to note that companies that fall under the NFRD scope when countries transpose the Directive to their national laws, will not be required to report the Taxonomy figures.

How does the NFRD affect asset owners and asset managers?

Financial undertakings (here referred to as “asset managers,” for simplicity) need to exclude all non-NFRD investee companies (or “undertakings”) from their entity-level disclosures. This means that asset managers need to identify which company falls under the NFRD scope, and include those in their EU Taxonomy KPIs calculations (based on revenues, Capital Expenditures and Operating Expenses).

How can asset owners and asset managers solve for NFRD?

Clarity AI has developed a robust NFRD identifier that accurately labels which company falls under the NFRD scope using the thresholds defined in the Directive. Clients will then be able to recalculate the alignment of their portfolio to the EU Taxonomy by taking into account only NFRD companies at the push of a button.

Our advanced technological capabilities put Clarity AI in the best position to quickly react and adapt to any changes in the regulation or any additional guidelines made available by the European Commission.

Contact us to learn more about our EU Taxonomy solution and to request a demo.