Banking remains one of the most heavily regulated sectors in the world, and its ESG disclosure requirements continue to evolve. Case in point: the introduction of the European Banking Authority’s (EBA) EU Pillar 3 ESG disclosures has raised the bar for transparency and accountability across the sector.

In this vein, the EU recently approved updates to the Capital Requirements Directive (CRD) and the Capital Requirements Regulation (CRR), known as the EU Banking Package. With these amendments, ESG disclosure requirements will now extend beyond the current list of approximately 80 Systemically Important Financial Institutions (SIFIs) to include over 2,000 Less Significant Institutions (LSIs), with a proportional approach for smaller institutions, and will start applying in January 2025.

These Pillar 3 ESG disclosures are part of the EU’s implementation of the three pillars of the Basel III Accord, a set of international banking regulations developed by the Basel Committee on Banking Supervision (BCBS) to strengthen the regulation and risk management of banks.1 They provide critical insights into banks’ capital and liquidity adequacy and risk management practices.

Figure 1. Basel III Pillars

Source: EBA

Importantly, the EU’s Pillar 3 guidelines rely on well-established global ESG frameworks to standardize sustainability data reporting and help close gaps in the banking sector’s ESG disclosures.

Upon the release of the standards in 2022 the EBA stated that the “ESG Pillar 3 package will help to address shortcomings of institutions’ current ESG disclosures at EU level by setting mandatory and consistent disclosure requirements.”

The message for the banking sector is clear: it’s essential to ensure your sustainability data and reporting standards are sufficient to meet these updated requirements. By doing so, you’ll also be ensuring you align with broader sustainability reporting obligations.

What Is Included in the Pillar 3 ESG Disclosures?

Key Components: A Closer Look at Qualitative and Quantitative Dimensions

The Pillar 3 reporting standards require banks to provide both qualitative and quantitative information to offer a complete view of how they manage ESG risks. These components work together to give stakeholders a detailed understanding of a bank’s strategy and its exposure to climate-related risks.

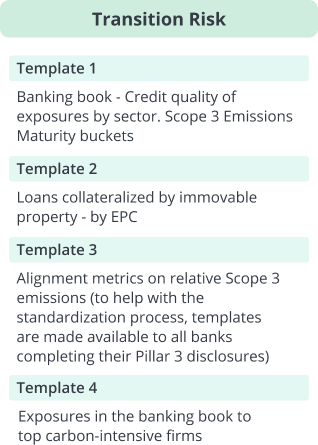

Pillar 3 includes 10 pre-defined reporting templates covering transition risks, physical risks and mitigating actions.

Figure 2. Pillar 3 Reporting Templates

Source: Clarity AI. For informational purposes only.

The role of EU Taxonomy in Pillar 3: Understanding the Green Asset Ratio (GAR) and Banking Book Taxonomy Alignment Ratio (BTAR)

The Pillar 3 ESG disclosures require banks to disclose both their GAR and BTAR. Both are measures of consistency between a company’s financing activity and the EU Taxonomy.2

The GAR focuses on exposures to companies reporting their taxonomy alignment, whereas the BTAR covers those exposures to companies not reporting their Taxonomy alignment (e.g. non EU companies, SMEs). Taken together, GAR and BTAR are an important tool for sustainability professionals because they demonstrate how well the bank is aligning its financial assets with sustainability objectives, such as climate change mitigation and adaptation.

Sourcing Reliable Data for Accurate Pillar 3 ESG Disclosures

Gathering reliable ESG data is essential for fulfilling the Pillar 3 obligations. To meet these requirements effectively, banks must ensure that their ESG data is both accurate and comprehensive.

The implementing standards emphasize the importance of a ‘best-effort basis’ approach when collecting ESG data. This means banks are expected to go beyond mere compliance, and actively strive for high-quality, granular data that can withstand scrutiny from regulators and stakeholders alike.

Quality ESG data serves as the backbone for informed decision-making, as it allows institutions to better assess their exposure to risks like climate change, social unrest, and governance failures. Moreover, reliable data enables banks to measure their progress toward sustainability goals and ensure that their disclosures are aligned with established regulations and standards, such as the EU Taxonomy and the Task Force on Climate-Related Financial Disclosures (TCFD).

As the regulatory landscape continues to evolve, sourcing high-quality ESG data will remain a key priority for financial institutions, helping them not only to comply with current requirements but also to build trust with investors and regulators by demonstrating their commitment to sustainability.

The Importance of Carbon Emissions in ESG Reporting

Carbon emission reporting plays a central role in ESG frameworks, including within the Pillar 3 requirements. High-quality carbon emissions data is not just a regulatory requirement. It provides valuable insight to investors and customers, allowing them to evaluate a bank’s financial stability, risk profile, and overall sustainability.

Under the Pillar 3 ESG disclosures, banks are required to detail their plans for reporting their Scope 1, 2, and 3 financed carbon emissions. However, while nearly 80% of companies in the MSCI All Country World Index (ACWI) have disclosed their scope 1 and 2 emissions, only 60% have reported at least some of their scope 3 emissions. This is partly because scope 3 emissions remain the most complex and challenging data to collect, as it covers indirect emissions across a company’s value chain—an issue that impacts all sectors, including banking.

As the pressure to provide comprehensive carbon emissions data grows, banks must develop robust systems for collecting, calculating, and reporting this information, particularly scope 3 emissions. This is vital not only for regulatory compliance but also for meeting the expectations of stakeholders who are increasingly concerned about the climate impact of financial institutions.

Pillar 3 ESG Disclosures and Market Expectations

Forward-thinking sustainability teams across the banking sector are ensuring their sustainability reporting function is ready and optimized to meet the Pillar 3 requirements along with their other sustainability reporting obligations.

By incorporating high-quality ESG data into a consistent and repeatable reporting framework, banks can deliver reliable and comprehensive disclosures. This approach not only satisfies regulatory obligations but also provides meaningful insights for investors, regulators, and customers, fostering trust and demonstrating a commitment to long-term sustainability.

How Clarity AI Can Help

| Banking Book Taxonomy Alignment Ratio (BTAR) | Clarity AI can help with reporting standard alignment discrepancies as highlighted by a bank’s BTAR. Clarity AI’s Climate solutions include data and insights to assess and benchmark alignment with Net Zero and Paris Agreement frameworks, as well as all quantitative TCFD-related disclosures. |

| Sourcing Reliable Data | Clarity AI is committed to providing the highest quality ESG data for clients to confidently analyze and report on sustainability. This is possible through a powerful, scalable technology, trained by a global team of sustainability experts and data scientists. |

| EU Taxonomy Data Coverage | Clarity AI’s coverage of reported data is the highest in the market with over 2,000 private and public companies, including eligibility and alignment percentages. Users can access the company report where the data was retrieved through a direct link. The additional BTAR dataset leverages our entire EU Taxonomy universe of more than 65,000 companies. By providing a country and NACE Code mapping, clients are able to easily prepare the table for the template 9. |

| Carbon Emissions Reporting | Clarity AI’s CO2 emissions data coverage is up to three times more than other providers. High-quality Scope 1, 2, and 3 data, both reported and estimated, is available, along with full transparency regarding the underlying calculations. |

This article was originally published in December 21, 2022.

References

- Bank for International Settlements. Basel III: International Regulatory Framework for Banks. Accessed: October 3, 2024. https://www.bis.org/bcbs/basel3.htm

- Commission Implementing Regulation (EU) 2022/2453 of 30 November 2022 amending the implementing technical standards laid down in Implementing Regulation (EU) 2021/637 as regards the disclosure of environmental, social and governance risks . https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv%3AOJ.L_.2022.324.01.0001.01.ENG&toc=OJ%3AL%3A2022%3A324%3ATOC#d1e34-16-1

Author Information