Exploring the US Securities and Exchange Commission Sustainability Related Proposals

Introduction:

The US Securities and Exchange Commission (SEC) recently confirmed expected dates for three proposed rules aimed at standardizing the approach to ESG practices, promoting transparency and preventing greenwashing in the investment industry. The rules, with one set to be finalized for April 2023 and the other two for October 2023, are poised to bring about a sweeping change in how asset managers and corporations approach sustainability. As the SEC intensifies its focus on ESG matters, market participants must prepare themselves to ensure they are ready for the upcoming changes. Clarity AI aims to provide some clarity in light of these complex rule changes, and can also assist by offering products that can help investors navigate these changes.

Background:

As a response to the growth in sustainable investing, the SEC has proposed three specific rules which seek to enhance both accuracy and transparency of disclosures in non-financial corporations and funds to enhance transparency and ensure investors receive adequate protection from greenwashing. The rules set to revamp the existing framework include:

- Proposal for Climate-Related Disclosure Rules for Public Companies

- Proposal for ESG Disclosure Rules for Investment Companies and Advisers

- Proposal for Rule to Address Misleading Investment Company Names

The first rule applies to public companies registered with the SEC. The second and third rules apply to investment funds and advisers.

These proposed rules are not finalized yet and may be subject to changes or legal challenges prior to their implementation. Nonetheless, they will engender new requirements on the industry and it is important market participants begin to prepare for their implementation.

Climate disclosures for Companies:

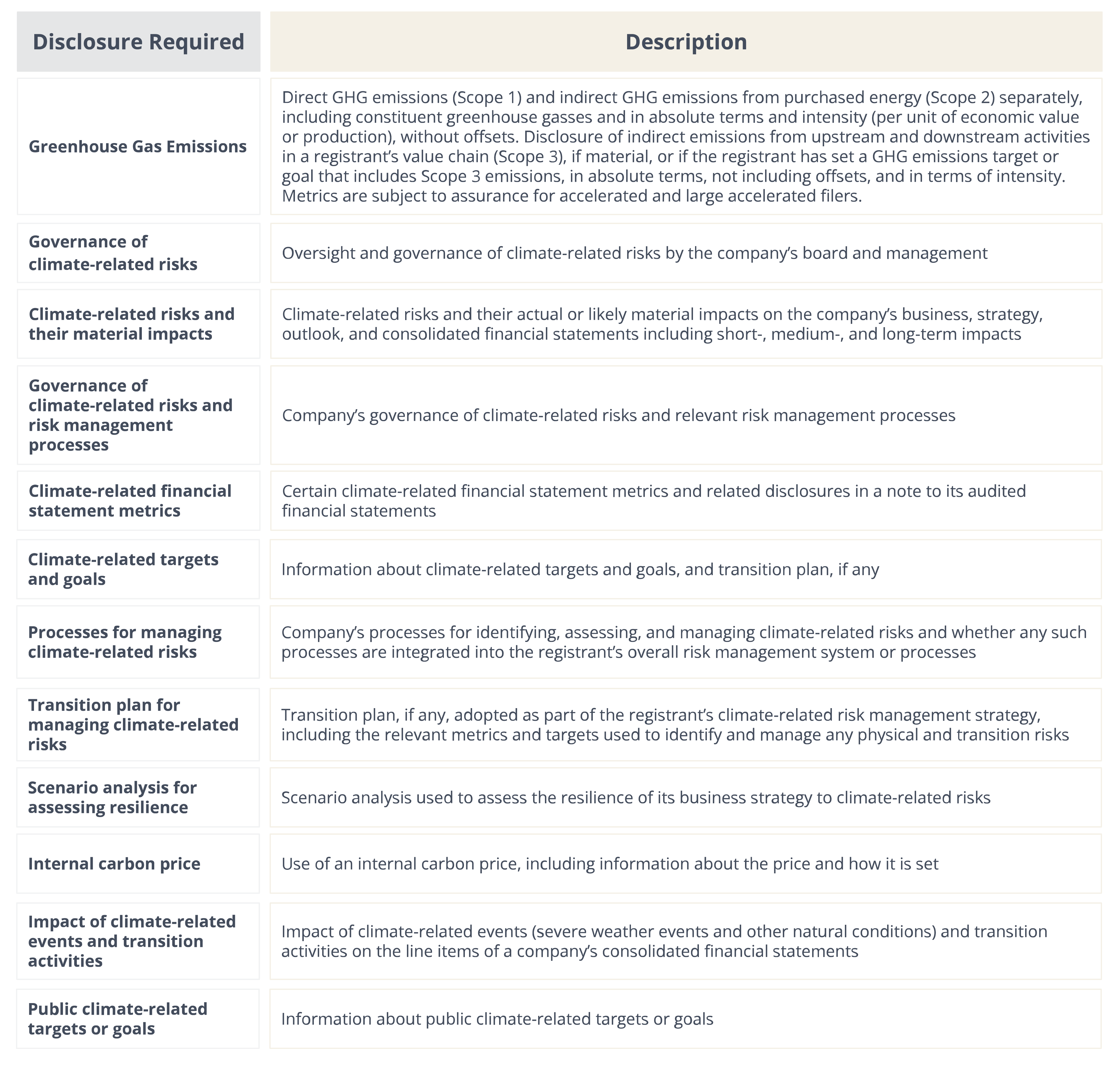

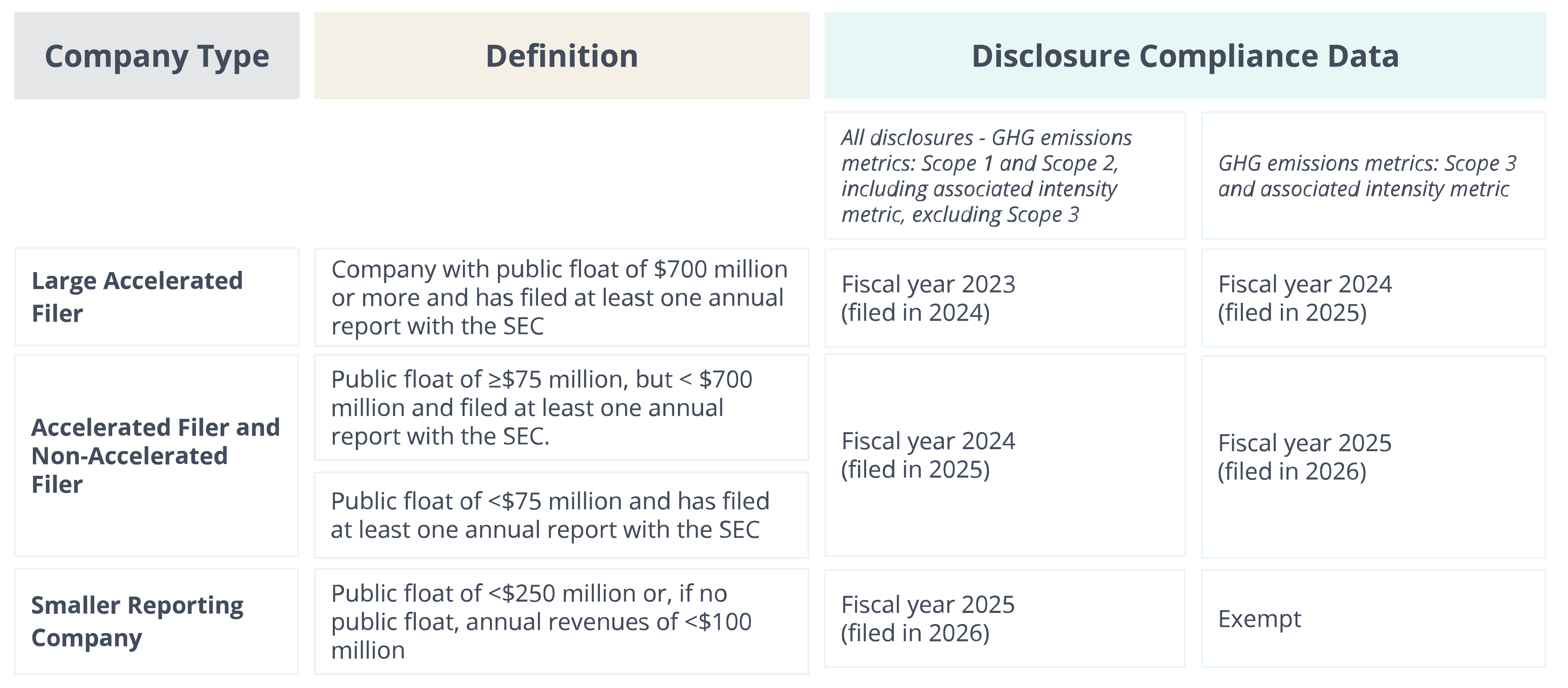

In March 2022, the SEC proposed rules for public companies to disclose their environmental and climate-related risks. The recent SEC communication confirmed these proposed rules will be finalized for April 2023 and begin coming into force by 2024. The rules – based on recommendations from the Task Force on Climate-Related Financial Disclosures (TCFD) – aim to standardize and enhance current non-financial disclosure practices, which have been deemed insufficient and inconsistent. The proposed rule requires mandatory disclosure of climate-related information which includes Scope 1 and 2 and, “if material”, Scope 3 greenhouse gas emission data by SEC registrants. This implies that companies will need to measure both their own emissions, and also report data from companies in their supply chains. The proposed rule also includes scope for collecting information on the registrant’s governance, strategy and risk management. It is expected that the proposals will align with the International Sustainability Standards Board (ISSB) proposed standards for climate related disclosures. See below the key features of the proposed requirements.

Disclosure Presentation:

The proposed rules require that the disclosures are presented in a clear and understandable manner, in a separate and appropriately labeled section of the registration statement or annual report (as per Regulation S-K). Furthermore, climate-related financial metrics should be included. The proposed rules require both qualitative – description of risks, impacts and opportunities – and quantitative climate-related disclosures. The quantitative metrics must be tagged in line with XBRL.

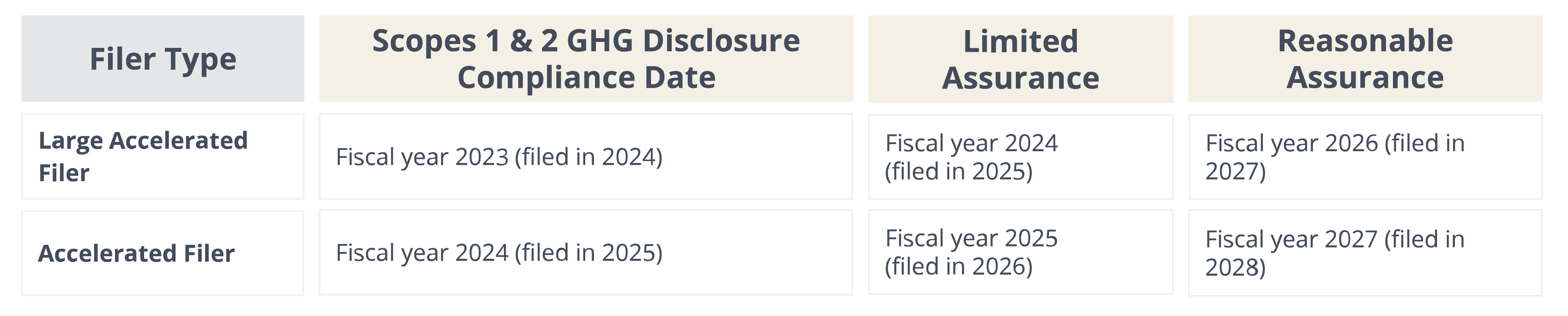

Accelerated filers must get an attestation report from an independent attestation service provider covering Scopes 1 and 2 emissions disclosure. The proposal does not offer any specific guidance on how to calculate these metrics, but requires companies to use “reasonable methodologies.”

These are the proposed phase-in periods for accommodating the disclosures:

Fund disclosures:

The SEC also proposed rules in the form of amendments to the Investment Company Act of 1940. The amendments will require asset managers to disclose additional information pertaining to their ESG investment practices and the SEC is proposing three different categories of funds to reflect different types of sustainability related objectives. These requirements, which are to be finalized by October 2023, aim to provide consistent information on strategy and ESG investments for end investors. The proposed amendments only apply to those who use an ESG label or consider ESG factors in their investment process. Funds who do not incorporate ESG factors or opt not to disclose information are not mandated to do so under the proposed amendments. These requirements are comparable to SFDR (which includes Article 6, Article 8 and Article 9 funds) and the UK’s SDR proposal (which consulted on ESG Focus, Impact and Improver labels).

Proposed Amendments:

The proposal identifies three types of ESG funds:

The table below is provided in the regulation and supports strategy disclosures by ESG-Focused Fund:

Name Rule for Funds:

In May 2022, the SEC also proposed amendments to the Investment Company Act Names Rule, in order to prevent fund names from misleading investors about a fund’s investments and risks. These rules are aimed at investment funds using ESG terms in their names and are to be finalized by October 2023.

Proposed Amendments:

The proposed amendment to the Names Rule expands the scope of the 80% investment policy requirement to any fund name which suggests a focus on any specific characteristics to cover ESG terms. The rule prohibits funds from using ESG or similar terminology in their name if ESG factors are not centrally considered in investment decisions. This means that funds using ESG or similar terminology would be required to invest at least 80% of their assets aligning with an ESG focus. This rule is in line with a proposal from ESMA to require Article 8 funds with ESG related-terms in their names to invest 80% in assets used to meet the environmental or social characteristics or sustainable investment objectives in accordance with the binding elements of the investment strategy.

What is next?:

The dates provided in the SEC’s rule making agenda are often more indicative than concrete. We do however expect all three rules to be finalized in the coming months. Nevertheless, there is a strong possibility of litigation, meaning a degree of legal uncertainty for companies. The inclusion of disclosures on e.g. Scope 3 emissions and other related issues could lead to judicial challenges.

Despite potential challenges, companies and asset managers should start preparing for the proposed rules in good time. This is important to ensure that asset managers and companies are prepared for the requirements. Finally, many fund managers may have already experienced the growing trend amongst end investors to demand non financial information. As such, providing information on the sustainability of companies within an investment fund in a formalized and standardized way may support customer demand for sustainability insights.

How can Clarity AI Help:

Clarity AI offers data-driven solutions with a range of technology-based products to deliver sustainability insights to its clients, such as those to help prepare for the SEC’s proposed rules:

TCFD & Climate Disclosures: we provide tools to measure, manage, and report performance by using industry-standard frameworks such as the TCFD. By quantifying GHG emissions, our clients can assess exposure to climate-related risks. Using our services allows market participants to achieve greater transparency in climate disclosures, including monitoring their portfolio against any net zero targets.

ESG-Risk: with our tools, asset managers can better understand ESG data and analysis, which leads to a more comprehensive assessment of portfolios. This data allows asset managers to make more informed decisions and to identify ESG risks more effectively. Equally, funds will be able to manage their ESG risk exposure to effectively reach investment objectives. This product might be useful for funds pursuing an ESG integrated strategy, and integrates a SASB approach to financial materiality.

ESG Impact: The tool could be used for funds pursuing an ESG impact strategy. Assess Impact on 10 sub-pillars across ESG to uncover a company’s inside-out exposure – Market leader in data coverage: Up to 2x times more companies coverage than competitors that assess ESG impact, with a universe comprising over 43k companies.

EU Regulation Modules: we offer regulatory products for businesses operating in Europe, including EU taxonomy, SDFR and MiFID II tools. These solutions allow customers to understand their portfolios alignment with sustainability criteria. Furthermore, Clarity’s tools provide valuable analyses on sustainable investments, allowing investors to identify insights on sustainable criteria and assess the impact of their portfolio on key factors.

If you have interest in exploring our solutions please contact us.