Are green bonds aligned with the EU Taxonomy?

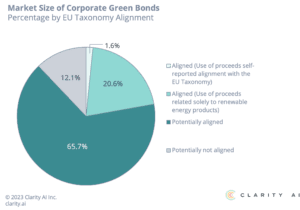

Clarity AI’s assessment of +17,000 green bonds finds that 22% are aligned with the EU Taxonomy

Green bonds are fixed income instruments that fund environmental projects. While they represent only a small percentage of the global bond market, their size is expected to exceed $2 trillion in 2023.

There is currently no legal definition of green bonds in Europe, so their issuance is based on voluntary standards such as the widely used ICMA Green Bond Principles. However, the European Union is developing (1) a new framework, the European Green Bond Standard (EU GBS), requiring the proceeds to be allocated to economic activities that meet the EU Taxonomy requirements. For now, investors can assess the EU Taxonomy alignment based on the use of proceeds, with the most common categories being renewable energy, green buildings, and clean transportation.

The EU Taxonomy requires large European companies to report the percentage of their activities that are aligned with an environmental objective, currently covering the objectives of Climate Change Mitigation and Climate Change Adaptation. Companies can only claim alignment if they I) are involved in an activity covered by the Taxonomy, II) meet the technical criteria for that activity, III) do not harm other environmental objectives, and IV) maintain minimum social safeguards. Similarly, asset managers can claim alignment with the Taxonomy if their funds invest in instruments that are aligned with the EU Taxonomy. They can then use this information as evidence of the environmental characteristics or objectives of their financial products.

The EU Taxonomy regulation does not apply to bonds issued by sovereigns, supranationals, or agencies (SSAs) as the EU Taxonomy alignment methodology for this type of issuer has not yet been defined. We anticipate that more clarity on this issue will emerge once the EU GBS is finalized.

As a result, our methodology for assessing EU Taxonomy alignment focuses on the use of proceeds of green bonds issued by companies. We consider a green bond to be aligned with the EU Taxonomy if either the issuer claims that the use of proceeds are aligned with the EU Taxonomy or if the use of proceeds is related solely to renewable energy.

We also deem a green bond potentially aligned if the use of proceeds is related to any of the following activities covered by the EU Taxonomy: green buildings, energy efficiency, or clean transportation; or if the use of proceeds lists more than one of the aforementioned categories. The designation of potentially aligned indicates that while we cannot guarantee that the use of proceeds for the green bond meets all the relevant technical screening criteria, we believe it is highly probable that they are met.

We consider the Do No Significant Harm (DNSH) criteria of green bonds to be met because green bonds standards already require a robust assessment of evidence of not harming the relevant environmental objectives. Finally, we evaluate whether the company meets minimum social safeguards following closely the recommendations of the Platform on Sustainable Finance.

After analyzing the EU Taxonomy alignment of over 17,000 green bonds, we have found that 22% of the corporate green bond market is aligned with the EU Taxonomy, primarily from those financing renewable energy projects. Most of the green bonds have multiple uses of proceeds, making it difficult to evaluate their alignment with the EU Taxonomy. As a result, we currently classify these cases as potentially aligned.

At Clarity AI, we stay up-to-date with the latest developments in the EU GBS to ensure that our solution aligns with the regulation. Adding green bonds helps ensure a more accurate picture of the sustainability profile of the portfolio and more accurate regulatory reporting. Please do not hesitate to contact us to learn more about our methodology or to arrange a custom demo for your organization.

1.) In fact, the Council and the European Parliament have recently reached a provisional agreement on a regulation that lays down the requirements to use the designation European green bond.

Related Posts

-

November 3, 2023 · 5 min readAI

November 3, 2023 · 5 min readAIAI’s Role in Making ESG Data More Reliable

AI can play an important role in providing quality data with automation and scale for asset managers’ ESG-minded client portfolios.

Learn More -

August 23, 2024 · 7 min readAI

The Next Frontier in Investment Management: GenAI for Smarter, More Efficient Portfolios

A case for integrating AI into sustainability data & analytics Generative AI (GenAI) could add to the economy between $2.6 trillion and $4.4 trillion annually while increasing the impact of artificial intelligence &#...

Learn More -

May 23, 2024 · 2 min readRegulatory Compliance

Regulatory Update: FCA’s Guidance on SDR’s Anti-Greenwashing Rule

Transcript: The FCA’s anti-greenwashing rule comes into force at the end of this month, May 2024. The accompanying guidance was only published at the end of last month, giving firms little time to make any necessary ad...

Learn More