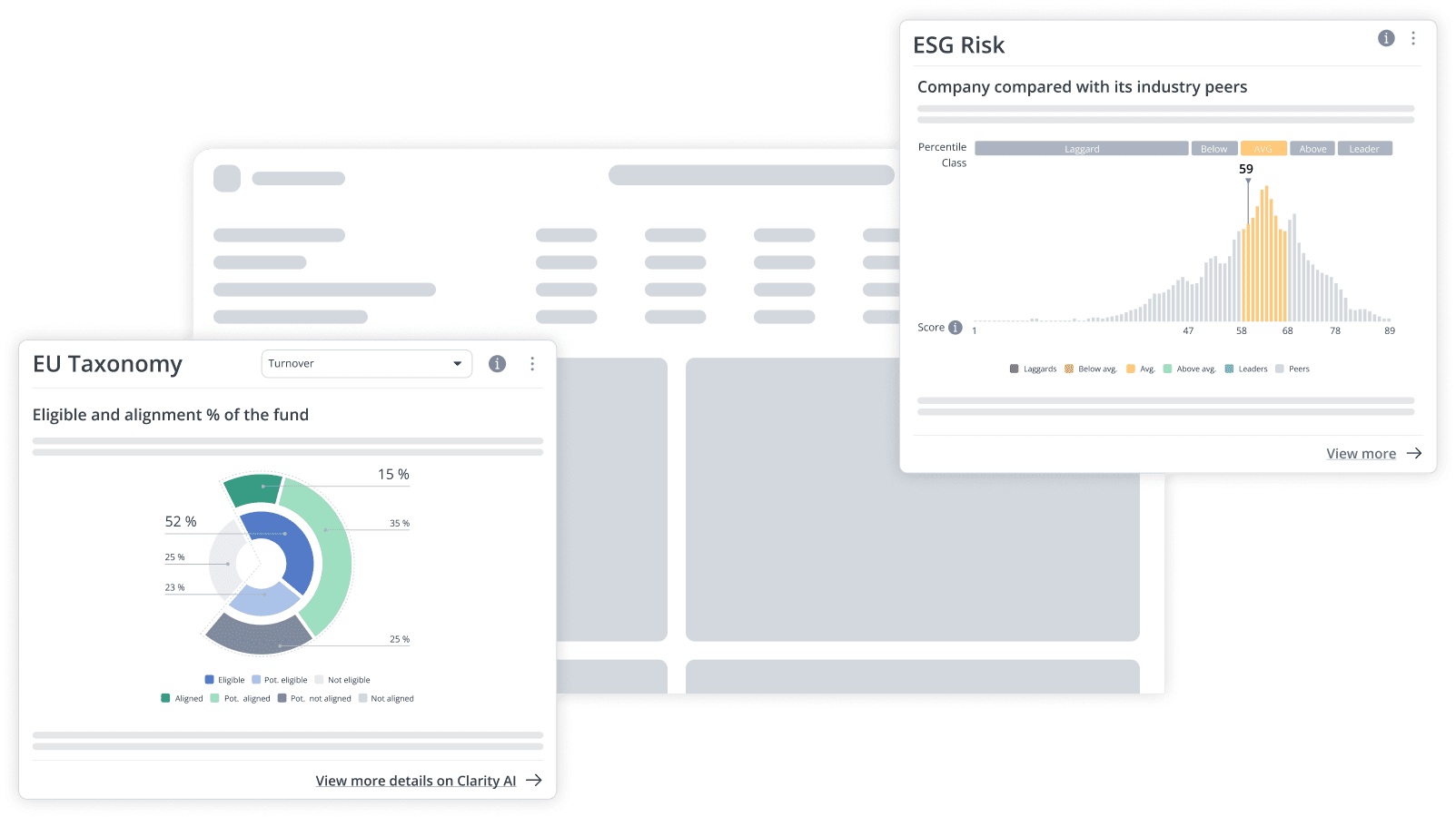

How Clarity AI’s EU Taxonomy solution can help you distinguish data types

Together, the EU Taxonomy and SFDR regulations create rules for how financial market participants (mainly asset managers) have to disclose sustainability-related information. For example, asset managers offering financial products that promote environmental characteristics (Article 8) or objectives (Article 9) have to disclose how their products are aligned with the EU Taxonomy. To do this, they can either collect the necessary information themselves or rely on third-party providers, such as Clarity AI.

This can be a challenge for asset managers as they find themselves questioning how to accurately interpret the data, how to mix data sources reliably, and how to build the analytical tools necessary to generate the required output. On top of that, there are questions around what information can be used and when, as the regulator distinguishes between reported, equivalent and estimated EU Taxonomy data.

Reported, equivalent, or estimated data: What are they and how are they different?

Reported data

Companies that fall under the Non-Financial Reporting Directive (NFRD) are required to report, over the course of 2022, their Taxonomy eligibility for the objectives of Climate Change Mitigation and Climate Change Adaptation. Soon after, over the course of 2023, they will need to report their eligibility and alignment for all six environmental objectives¹. This is what the regulator considers reported information.

How does Clarity AI present reported data?

Thanks to our technology and our focus on systematic tools, we can incorporate EU Taxonomy data reported by companies very quickly. Since reported data is the best type of data, we give it prevalence over any other information we may have on a company. We also make it evident to the user that this data comes from a report, including the appropriate tag and a link to the report itself when it applies.

Equivalent data

Since not all companies are reporting EU Taxonomy data, and many are not under the scope of NFRD, asset managers “may rely on equivalent information on taxonomy alignment obtained directly from investee companies or from third party providers”.

Equivalent data is information disclosed that is similar/analogous to the data expected by the regulation.

How does Clarity AI interpret and apply equivalent data?

In our EU Taxonomy solution, we use equivalent data that matches the technical criteria to generate an eligibility or alignment result for those companies for which we do not have reported data. We also treat as equivalent the contribution of eligible activities that have no technical criteria at all (such as electricity generation from wind).

Estimated data

The regulator considers estimated data the information that is derived from reasonable assumptions. In other words, it refers to all information that is neither reported nor equivalent.

How does Clarity AI interpret and apply estimated data?

At Clarity AI, we use estimated data in three main ways:

- Data reported by the company that perfectly matches technical criteria, but for which we have used proxies/estimations to calculate the associated revenue percentage. For instance, a company may disclose the number of electric vehicles sold but not the associated revenue, so we would have to estimate the average unit price to arrive at that figure.

- Data reported by the company that partially matches technical criteria. For instance, a steel producer may disclose the carbon intensity of its production but not the manufacturing process used, so we estimate the applicable technical threshold using the information available.

- Proxies based on sector averages from academic research. For instance, we may learn from the academic literature that cement producers are unlikely to meet the EU Taxonomy’s carbon emission thresholds before 2040.

In all three cases, our output will be qualified as “potential” (“potential contribution”, “potential alignment”, etc.) to make it evident to the user that we are relying on reasonable assumptions to generate our results. We also make our sources available for clients so they can understand how we arrive at our estimates.

When can asset managers use estimated data?

The EU Taxonomy regulation states that, for the “exceptional cases where financial market participants cannot reasonably obtain the relevant information to reliably determine the alignment (…), they are allowed to make complementary assessments and estimates on the basis of information from other sources” (Taxonomy Regulation 2022/852). We interpret this as a limitation to using estimates only in certain cases, and not in a generalized way. It is worth noting that asset managers, insurers and credit institutions under NFRD (referred to as financial undertakings) may use estimates in their voluntary entity-level disclosures (European Commissions’s Article 8 FAQ document).

How are the different data types used?

To ensure compliance for regulatory reporting, we include a template generator that populates the EU Taxonomy alignment of a given portfolio based only on reported and equivalent data.

When our results are presented with a “potential” qualifier, it means that the information is based on estimates. This type of information can help asset managers anticipate the alignment of issuers expected to disclose equivalent or Taxonomy-specific information, or to measure the extent to which a portfolio is positively impacting environmental objectives, even if regulatory reporting is not the main focus.

¹The six environmental objectives of the EU Taxonomy are: Climate change mitigation; Climate change adaptation; Sustainable use and protection of water and marine resources; Transition to a circular economy; Pollution, prevention and control; and Protection and restoration of biodiversity and ecosystems