Nuclear power and fossil gas are now part of the EU Taxonomy reporting

On January 1st, 2023, six new activities related to nuclear power and fossil gas officially became part of the EU Taxonomy (1). Companies eligible for those activities are now able to claim alignment with the environmental objectives set by the taxonomy if these activities I) meet the technical criteria), II) do not harm other environmental objectives, and III) maintain minimum social safeguards.

The new regulation not only affects companies, but investors as well: Financial Market Participants (asset managers) can now consider fossil gas and nuclear activities as part of their EU Taxonomy fund disclosures.

In this article, we discuss the technical criteria for fossil gas generation and how its inclusion impacts investor portfolios. We focus on activity 4.29, Electricity generation from fossil gaseous fuels, because it is both the largest (it represents close to 60% of associated listed company (2)) and the most controversial activity in the new delegated act.

New Disclosures for Companies Under NFRD

Starting January 2023, NFRD companies have to report the percentage of their activities that are eligible and aligned with the EU Taxonomy, including their alignment with the new nuclear and fossil gas activities.

On top of the debate on whether fossil gas or nuclear should be considered green or even transitional, companies and market participants have to deal with the uncertainty of how to interpret the technical criteria. This particular criterion related to gas- powered generation has probably made the most noise:

I) “direct GHG emissions of the activity are lower than 270g CO2e/kWh of the output energy”

or

II) “annual direct GHG emissions of the activity do not exceed an average of 550kg CO2e/kW of the facility’s capacity over 20 years;”

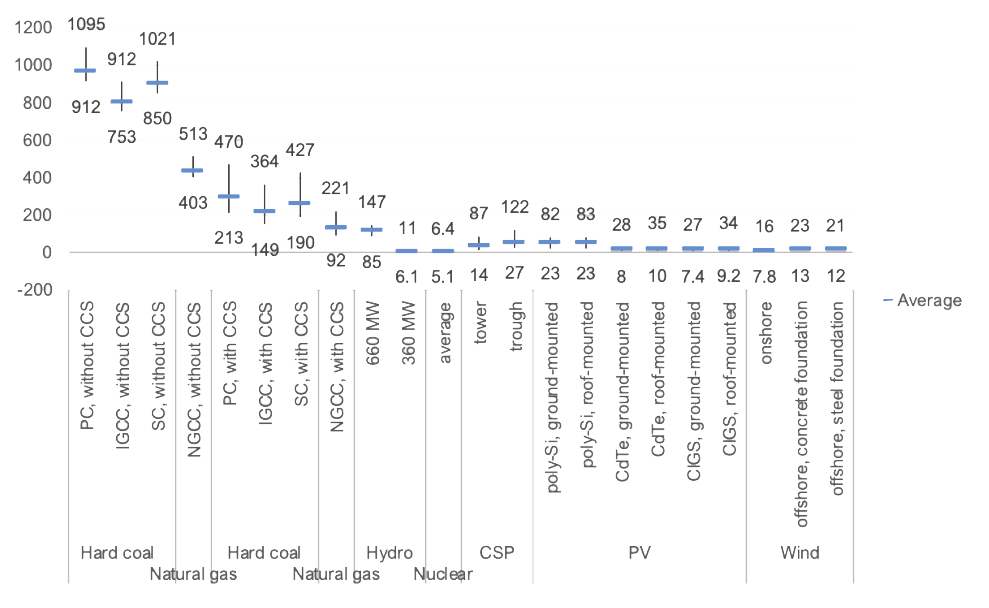

The first threshold of 270g CO2e/kWh is clear. Yes, it is higher than the general threshold of 100g CO2/kWh that applies to all other electricity generation technologies (an issue covered in detail by the Platform on Sustainable Finance), but at least it’s straightforward to measure and contrast. We can compare it with industry figures, and conclude that few companies (if any at all) will be able to meet the threshold, as the carbon intensity of this technology sits in the 403-513g CO2e/kWh range (3):

The main source of uncertainty, then, is the 550kgCO2e/kW threshold that is measured over the average of the next 20 years. This threshold creates interpretational and methodological challenges. In particular:

– The metric is based on a multi-year average which, by definition, cannot be precisely measured until the whole period has elapsed, forcing reporting companies to use estimates based on expected trajectories that need to incorporate several assumptions related to future electricity demand, technology development, and electricity mix in the region. These estimates will then need to be verified by independent third parties that will certify whether they are reasonable or not, based on their own separate estimates (4).

– The metric is based on capacity, not generation, so in a way, it is rewarding large, underutilized plants that could now be aligned with the EU Taxonomy instead of being decommissioned. For example, the large Alessandro Volta power plant in Italy has a capacity of 3.6 GW. Because the plant is underutilized (it runs just 30% of the time) it could meet the EU Taxonomy threshold because the carbon it emits is low in relation to its capacity (5).

– Similarly, capacity-based measures result in widely different performances across time for a given asset (utilization can vary widely across years (6)), making it difficult for investors to track and understand progress in terms of green technology investment. For instance, a plant may operate at 60% capacity one year and 40% capacity the next due to a number of external reasons (such as the supply of other energy sources), resulting in a lower CO2 kg/Kw value, potentially moving a power plant from “not aligned” to “aligned” with the EU Taxonomy as it crosses the threshold from one year to the next.

How Does It All Impact Investors?

An important criterion for fossil gas-related activities, and one that is also shared with nuclear power-related activities, is that the activity takes place within the European Economic Area (7). As a result, investors with exposure to electric utilities outside Europe will have zero Taxonomy-alignment from these activities.

For European utilities, however, and given the uncertainties mentioned above, it will be difficult to know what alignment numbers companies will finally report. Our expectation is that companies will report little to no alignment to the EU Taxonomy as they (and their independent third-party verifiers) follow the UN’s precautionary principle, embedded in European Union law and applicable to environmental regulations. This principle can be summarized as when in doubt, err on the side of the planet. More specifically, it transfers the burden of proof to the “producer or manufacturer who may be required to prove the absence of danger (to the environment)” (8).

At Clarity AI, we follow these developments closely to make sure that our solutions fully align with the latest version of the regulation. Contact us to see our EU Taxonomy data in action.

(1) The activities included in the Complementary Delegated Act (CDA) are:

- 4.26 Pre-commercial stages of advanced technologies to produce energy from nuclear processes with minimal waste from the fuel cycle

- 4.27 Construction and safe operation of new nuclear power plants, for the generation of electricity or heat, including for hydrogen production, using best-available technologies

- 4.28 Electricity generation from nuclear energy in existing installations

- 4.29 Electricity generation from fossil gaseous fuels

- 4.30 High-efficiency co-generation of heat/cool and power from fossil gaseous fuels

- 4.31 Production of heat/cool from fossil gaseous fuels in an efficient district heating and cooling system

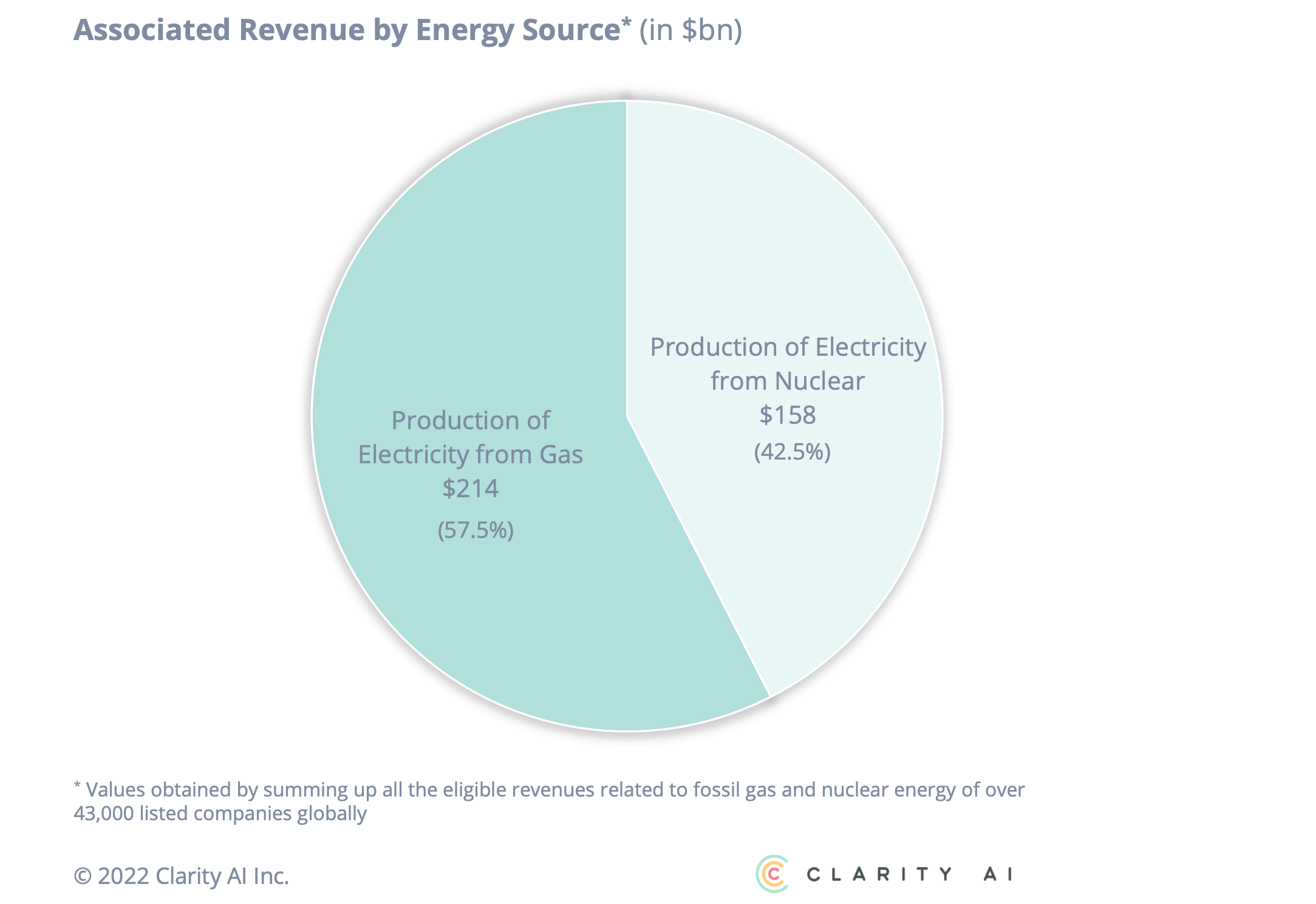

(2) Values obtained by summing up all the eligible revenues related to fossil gas and nuclear energy of over 43,000 listed companies globally

(3) Carbon Dioxide Emissions From Electricity – World Nuclear Association. Calculation of direct CO2 emissions for a typical conventional CCGT of 350 gC02e/kWh (according to IPCC AR5 WG3 Annex III, 2018)

(4) Commission Delegated Regulation (EU) 2022/1214

(5) Asset level data is notoriously hard to find in this industry, but some available figures suggest that this plant operates at around 280 kgCO2/kW capacity, well under the EU Taxonomy threshold

(6) Average capacity factors can range from 40 to 60% within a year even in large interconnected markets: U.S. Energy Information Administration – EIA – Independent Statistics and Analysis

(7) The criterion in all six nuclear and fossil gas activities states the following: “the project related to the economic activity (‘the project’) is located in a Member State”

(8) Treaty on the Functioning of the European Union – Article 191